Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

February 21, 2012

Supply Driven Pork and Beef Markets Hold Promise– By all expectations, 2012 is shaping up to be a very good year for U.S. pork producers, following a two-year recovery period. Many are still rebuilding. Even with historically high cost of production, we seem to be in a demand market scenario, which is giving producers an opportunity to lock in some very good returns for the remainder of the year.

I believe the market has factored in key items that drive the futures prices being offered. How those play out over the coming year will reveal how the market will respond relative to current futures levels.

USDA is projecting pork supplies to increase by 1.3% in 2012. This would seem to be a manageable supply if pigs grow normally during the summer and we don’t get them bunched up in the final quarter of the year. USDA projections estimate that exports will be off by 2% in 2012, still giving us a manageable increase in domestic pork supply of 2.2%. Figure 1 provides a long-term and a short-term forward look at domestic pork supplies by reducing U.S. pork production by the export volume, net of pork imports. The critical message here is the significant reduction in pork supplies from 2009 to 2011, mostly due to growth in pork exports; 2011 was the smallest domestic supply of pork available in more than 10 years, which gave us record high average pig prices.

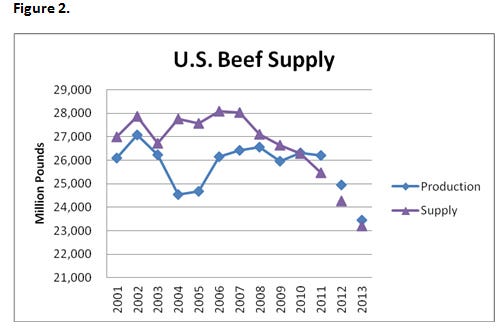

I believe that U.S. beef supply will be supportive to pork prices (Figure 2). Initially higher feed costs followed by drought throughout much of the south and southeast have continued to reduce the beef cow herd. USDA projections of beef supplies indicate the dramatic reduction. This situation should be very supportive of pork prices, which are at least in part built into the futures prices of pork.

Based on the USDA numbers, domestic pork supply will be down 7.1% in 2012 compared to five years earlier. Domestic beef supply will be down 13.4%.

Grain Price Volatility – Cost of production will continue to be high relative to long-term costs, but based on futures prices, will continue to trend downward and remain less than the last half of 2011. All one can say for sure is that grain prices will be volatile, depending on spring and summer weather. With much of the western Corn Belt lacking subsoil moisture, timely rains (or lack thereof) will drive cost of production. Many of our clients have taken advantage of the “forward crush” and locked in a percentage of their production needs. It is hard to pass up what the market is offering, at least on a portion of their production.

Temptations to Expand– Expansion in the pork sector is inevitable. History tells us that producers tend to put earnings back into more production. Someone told me a long time ago: “The cure for low prices is low prices.” The same is true for high prices or profits. Inevitably, the pork industry will over-produce. We always have. The major change from historical cycles is that our industry is significantly more volatile today. In recent years, corn prices and feed costs can and have changed more in a few months than they did in previous decades. This volatility requires your business to have more working capital reserves. The more astute managers of any business have recognized this need and have responded by working hard to build a strong business financial model. Those folks are your competition!

You May Also Like

Current Conditions for

70°F

Partly Sunny

Day 72º

Night 50º

Enter a zip code to see the weather conditions for a different location.