Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

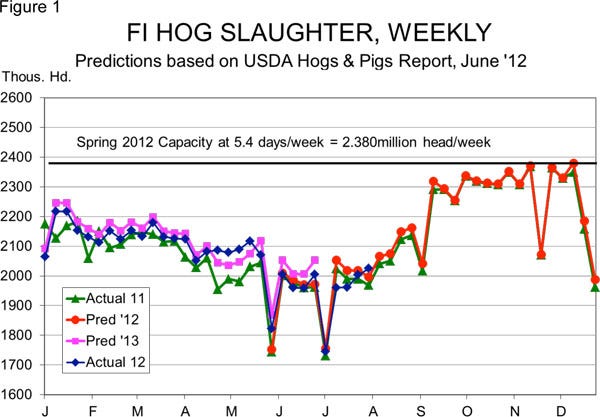

Estimated federally inspected (FI) hog slaughter was higher than one year ago for the second straight week last week, and exceeded the level predicted by the June Hogs and Pigs report for only the third time since June 1.

August 6, 2012

Estimated federally inspected (FI) hog slaughter was higher than one year ago for the second straight week last week, and exceeded the level predicted by the June Hogs and Pigs report for only the third time since June 1 (Figure 1). Last week’s 2.025 million head was the highest weekly total since mid-May and is right on cue to mark the normal seasonal upturn for U.S. hog slaughter. Cumulative weekly slaughter since the week that ended June 8 has been 17.623 million head, 0.9% less than the level predicted by the June report and 0.1% more than one year ago.

What does this imply for slaughter the rest of 2012? I think it says the levels predicted by the June report are still the best available estimates. They clearly show rising numbers in August, then the normal jump to around 2.3 million head per week come September. There could be a few hogs backed up by hot weather and resulting lower feed intake and growth rates, but average market weight data suggest that producers have been pretty aggressive about getting pigs to market. High and increasing feed costs have provided ample incentives to stay current. I’m still looking for Q3 slaughter to be down about 0.5% from last year, primarily due to there being one less week day in the quarter this year. Q4 slaughter will be up 2.0 to 2.5%, with much of that increase due to there being one more slaughter day in that quarter. The second half of 2012 should see slaughter that is about 0.8 to 1.0% larger on an average daily basis.

Weights the Wild Card

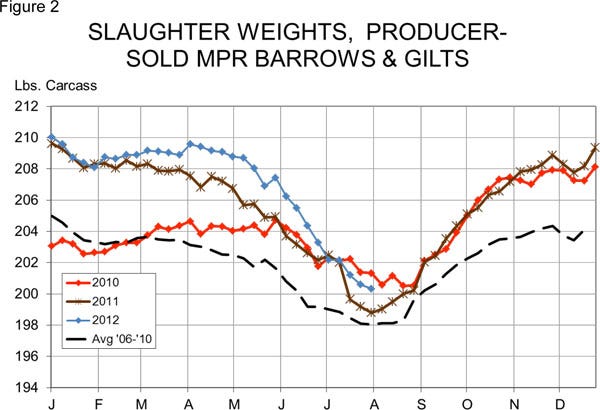

A relative wild card for the supply situation will be average weights. Top barrow and gilt weights have fallen faster and farther this year than normal due to the early onset of hot weather. Historically, 207-208-lb. carcasses in May should have been followed by 203-204-lb. carcasses in July and August. This year, the decline has been 6 to 7 lb. instead of 4 lb. Higher feed costs may have played into some of the July decline, but the rapid pace was in June when early heat hit.

Note that last week’s average weight of 200.3 lb. was lower than the week before, but that the rate of decline has slowed. As the black dashed line in Figure 2 shows, that is quite normal. The forecast of cooler temperatures this week and next may actually see weights hit their seasonal lows. If that holds true, I would expect weights to go no higher than 206 lb. or so this fall.

And they may not reach those levels as producers balance higher feed costs against seasonally lower hog prices. Any effort to save feed by reducing weights would support a lower Q4 peak for hog weights. Should top barrow and gilt carcass weights average 205.5 lb. in Q4, it would take a short 1% off of total pork supplies. Much of that reduction, however, may be replaced by high sow slaughter and sow product output.

Sow Sales

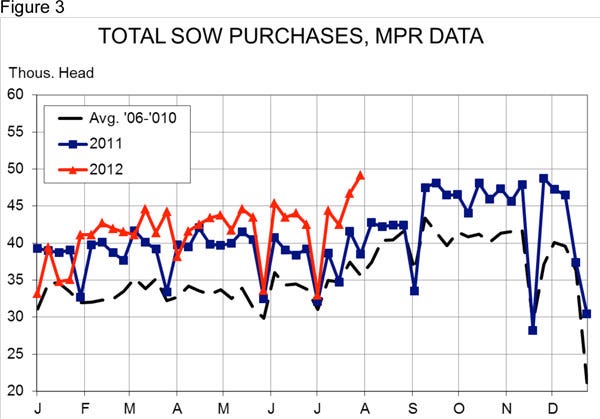

That brings us to our last point for this week. Last week’s sow purchase data through Thursday indicates that sow movement has indeed picked up. I estimate that the weekly total of sows purchased by those companies that slaughter more than 100,000 sows or boars per year (and thus must report price and quantity data to USDA) grew to over 49,000 last week, over 27% higher than one year ago (Figure 3).

That does not mean sow slaughter for last week will be 27% larger than last year when those data arrive in two weeks. The reason is that sow purchase numbers have exceeded year-ago levels and, thus, have been much closer to actual sow slaughter for much of this year. The increase in purchase numbers relative to last year in February or March suggests that a new company now qualifies for the Mandatory Price reporting (MPR) system. Purchase numbers now run about 13,500 less than slaughter where they once ran nearly 18,000 head per week under slaughter levels.

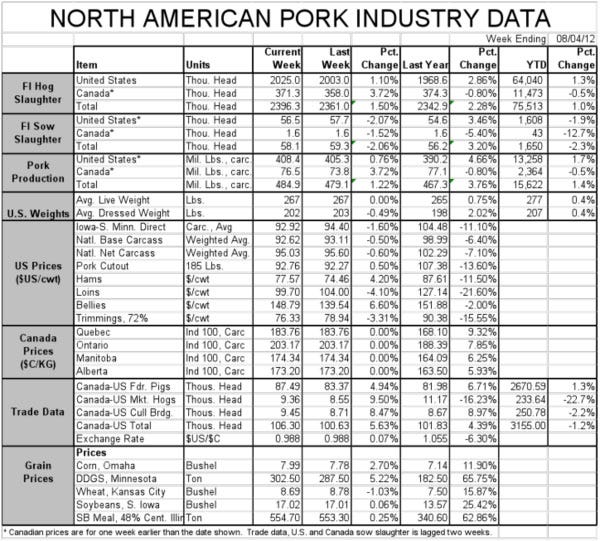

I expect FI sow slaughter to reach almost 64,000 for last week, though. That would be 13.7% higher than one year ago and signify the definite start of a liquidation and breeding herd reduction. It appears that another feed cost-driven supply reduction is underway.

Thanks for Your Concern

On a personal note, many readers know I hail from Oklahoma and some may have recognized Mannford, my home town, through a number of national news reports this weekend regarding Oklahoma’s wildfires. The Creek County fire did hit my parents’ home place, destroying a barn and some outbuildings, but sparing every structure of major value. My family is fine, but a number of friends and neighbors lost everything. I appreciate your concern and ask that you keep my fellow Okies in your thoughts and prayers.

You May Also Like

Current Conditions for

70°F

Partly Sunny

Day 72º

Night 50º

Enter a zip code to see the weather conditions for a different location.