Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

February 10, 2014

December export data is good news on two fronts. December’s U.S. pork exports provided a strong note on which to end a generally disappointing year. Total U.S. pork muscle cut exports for December amounted to 454.6 million pounds carcass weight equivalent, a total that was 6.5% larger than one year ago. That is only the second month of 2013 in which exports were larger than in 2012, and marks the largest monthly year-on-year increase since June 2012. 2013 annual exports of 4.992 billion pounds carcass weight equivalent will still fall short of the 2012 level by 7.2% but that figure is considerably better than the double-digit year-on-year shortfalls that prevailed for the first six months of 2013. The 2013 export total amounts to 21.5% of total estimated U.S. pork production. That figure is down from 2012’s record level of 23.1%.

The biggest factor for 2013 exports – Russia’s virtual withdrawal from the U.S. market – continued in December with no pork reported as being shipped there. Exports to Russia were 94% lower in 2013, with only small quantities being reported for January, February and, curiously, November. The decline in shipments to Russia accounted for 258,000 pounds of the year’s 388,000-pound reduction in exports. Viewed another way, had shipments to Russia been the same as in 2012, U.S. exports would have fallen by only 2.1% for the year. We have heard some talk that Russia has inquired about the ractopamine status of various U.S. packers and packing plants. That interest may well be driven by Russia’s recent banning of imports from the European Union (EU) over Lithuania’s African Swine Fever situation. It is winter in Russia and the masses have to eat something.

Like what you’re reading? Subscribe to the National Hog Farmer Weekly Preview newsletter and get the latest news delivered right to your inbox every week!

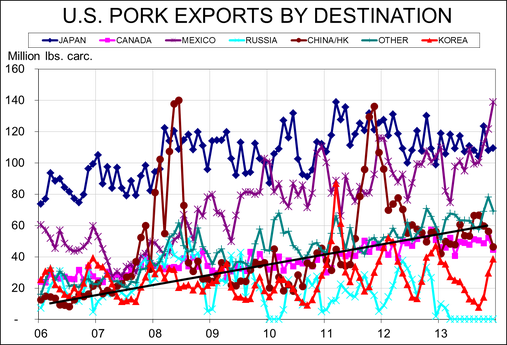

The biggest positive for 2013 is Mexico’s rise as a contender to Japan as our number one muscle meat destination. Mexico was the clear leader (see Figure 1) in November and December, and pulled to within 10 million pounds of Japan (1.3401 billion vs. 1.2405 billion) for the entire year on a carcass-weight equivalent basis. Exports to Mexico grew by 6.6% during 2013 while exports to Japan fell by 2.7%.

Figure 1

Mexico remained second in the list of U.S. pork variety meat markets for 2013. China/Hong Kong added to its status as the number-one destination for variety meats in terms of both tonnage and value. Variety meat exports to China/Hong Kong amounted to 192.3 million pounds valued at $392 million last year. Those figures are 13.4% and 20.2% higher than one year ago. Variety meat exports to Mexico fell by 1% in quantity and 5% in value in 2013.

Even with growth of our exports to Mexico, and the fact that Mexico virtually eliminated the gap between itself and Japan in 2013 in terms of the amount of pork taken from the U.S., we must realize that Japan is still far and away our leading market in terms of export value. Our muscle meat shipments to Japan last year were worth $1.842 billion while those to Mexico were worth only $979 million, just over half as much.

A primary driver of the high value of pork shipped to Japan, though, is the gate price system which basically requires that high value cuts comprise the lion’s share of export volume. That mechanism would almost certainly be eliminated by the Trans-Pacific Partnership (TPP) should it be implemented. The impact would be two-fold. First, the average value of the products going to Japan would fall since lower-valued products would eventually be allowed into that market without the onerous tariff equal to the difference between the product’s value and the gate price. But the flip side of that development is that lower-valued U.S. product that has been almost precluded from the Japanese market would then be allowed in without the tariff (or at least with a smaller tariff) thus increasing U.S. export volume.

The final two positive stories from the December data are the continued growth or our exports to “other” markets and some recovery of shipments to Korea. Other markets (primarily driven by Australia and a number of Latin American countries) again ranked third among all markets last month and ended 2013 as our third-largest export destination. This growth improves the diversification of our export market portfolio and makes us less vulnerable to export disruptions in specific markets. The month-to-month growth for Korea is primarily a normal seasonal pattern, but it is growth – something quite lacking for this market in early 2013. Our shipments to Korea are still down by nearly one-third but I’m hoping this late-year push is a harbinger of some improvement in 2014.

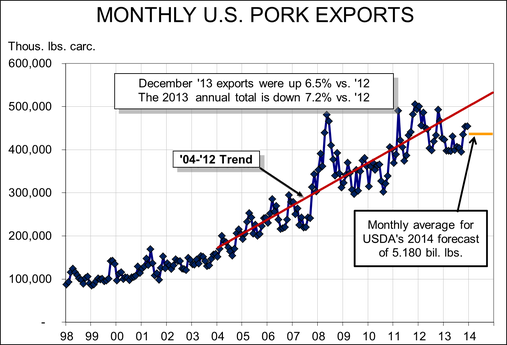

Can exports grow in 2014? I believe they can. USDA has pegged them at 5.180 billion pounds next year (see Figure 2). That level appears quite attainable, but there will be challenges. First, pork prices are going to be higher than we once expected due to porcine epidemic diarrhea virus (PEDV)-driven supply losses. Second, a generally stronger U.S. dollar has reduced the buying power of Japan’s yen and Mexico’s peso and hurt our competitive position relative to Canada and Brazil. The first two of those make U.S. pork more expensive relative to domestic supplies, while the latter two increase our product prices relative to Canada and Brazil.

Figure 2

U.S. pork is still a great value in most markets and I still believe the Smithfield-Shuanghui merger will push shipments to China/Hong Kong upward at a more rapid pace than the trend of recent years. Barring any huge disruptions, I expect another good year for U.S. pork exports.

You May Also Like

Current Conditions for

51°F

Mostly Sunny

Day 72º

Night 50º

Enter a zip code to see the weather conditions for a different location.