Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

January 6, 2014

Happy New Year! As 2014 dawns with a brutal cold rush, it is time to look at the economic issues that will be key to producers’ success this year and beyond.

The 2014 crop. “It’s baaaaaa---aaaack!” Actually, the issue of crop size has never left us since the dawn of the biofuel era. Last year’s record corn crop and near-record soybean crop have reduced the cost pressure on feed users but just how long will that last? The answer is, “Not too long if the 2014 crop isn’t another good one!” The EPA’s 2014 Renewable Fuel Standard (RFS) will require blenders to use roughly 13.5 billion gallons of corn-based ethanol. That decision puts less pressure on the corn supply than we have seen since 2004. In addition, other countries now produce about 50% more corn than they did in 2004 before the original energy law and the original RFS was set.

The corn supply has pretty much caught up with usage when corn is priced in the range of $4.00 to $5.50 per bushel. But total domestic usage and exports will now exceed 13 billion bushels any time we do not have a short crop. Corn acres will almost certainly be lower in 2014 due to high soybean prices. A harvested acres figure of 85 million bushels (versus 87.2 in 2013) and a trend yield of 162.1 bushels per acre would put the crop at 13.770 billion bushels, down 220 million from last year. Shave 10% off the yield, though, and you get 12.401 billion bushels and will very likely push carryout stocks back below one billion bushels and get corn prices in the $6.00 to $7.00 range. Feed supply, demand and cost are all better but still leave pork producers on the precipice of high costs.

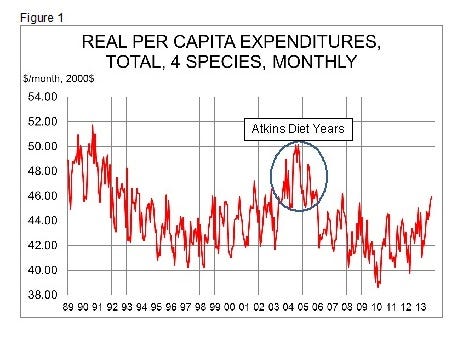

Pork – and meat – demand. This is on the list every year, of course, but we begin this year with more positive momentum since the early ‘00s. As can be seen in Figure 1, real per capita expenditures on the four major animal protein species were higher in October than in any month since 2005 except for September 2007. I think 2013 will be the best year for consumer spending on meat and poultry since 2005 when the November and December figures are all available in early February.

I think we need to consider the Atkins Diet years of 2004-2006 somewhat as “outliers” in Figure 1. While I am living proof that the concepts of the Atkins Diet are sound and will work to reduce weight and improve cardiovascular health, it was a bit of a craze that may constitute what amounts to anomalous readings for meat and poultry demand in those years. Remove those high observations and the chart looks far more continuous with the lows of 2009 and early 2010 driven largely by the Great Recession’s huge negative impact on the restaurant sector and a “trading down” impact on consumers’ choices at retail.

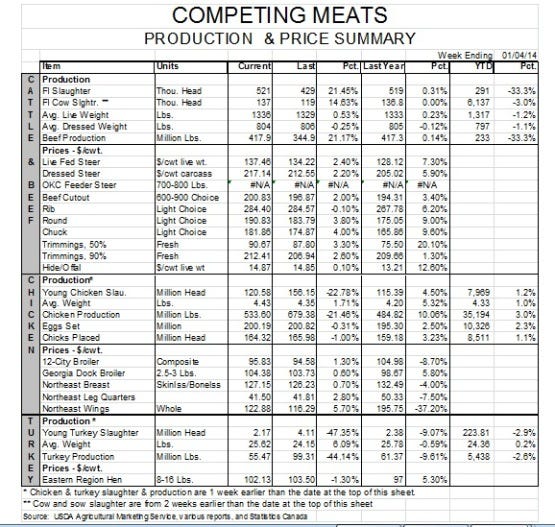

Per capita consumption of pork and broilers GREW by 1.8% and 1.6%, respectively in 2013, while it remained steady for turkey and fell by 1.8% for beef. But the expenditure driver is price. Strong demand has been revealed by consumers’ willingness to pay record-high prices. Will that continue in 2014?

Exports. Always an issue now that they represent nearly one-quarter of U.S. pork production and an even higher percentage of U.S.-Canadian output. Russia is still not taking U.S. pork and there appears to be no change in sight for that stance. Year-on-year comparisons for China-Hong Kong will look much better this year since we will be comparing to “normal” shipments which continue to trend upward very nicely.

There are two big risks. First, there is the ever-present danger of an export-blocking disease outbreak. Porcine epidemic diarrhea virus (PEDV) is proof that it could happen and is also proof that we may not be able to handle a more serious disease outbreak. I say “may” there only because PEDV, as a “non-reportable” disease, did not trigger all of the possible interventions available to federal and state regulators that foot and mouth disease, African swine fever or classical swine fever would trigger. Would the additional actions make a difference? I hope so but . . .

The second issue is, of course, what happens with the mandatory country of origin labeling (MCOOL) situation. We should know the World Trade Organization’s (WTO) take on the new US rule this spring. If they say it is sufficient (which I do NOT expect!), the program will stand and exert negative impacts on Canadian hog and cattle producers and Mexican cattlemen. If they agree with me and find the rule change insufficient, then the ball will be in the Congress’s court once again. We hear of a “fix” in the U.S. farm bill but have not seen the specifics. I find it very hard to believe that a country-of-origin labelling program that is not based on the long-sufficient idea of substantial transformation can meet trade commitments.

Like what you’re reading? Subscribe to the National Hog Farmer Weekly Preview newsletter and get the latest news delivered right to your inbox every week!

Hog numbers. This is always a factor, of course, but it is an obvious issue for 2014 given PEDV losses and the counter-intuitive figure for the U.S. breeding herd in the December Hogs and Pigs report. It appears now that 2014 annual slaughter will be roughly even with that of 2013. And, I think the estimates will get smaller as the true extent of PEDV losses becomes known. Higher weights will add to production and likely leave total U.S. output larger than last year – but not by much. Export and population growth will leave per capita availability lower by 1-2%, implying a continuation of strong hog prices.

In closing, I want to relate an experience from last week. My family and I attended the Rose Parade last week. Beautiful floats, terrific bands, lovely weather and 700,000 of our now-closest friends all added up to a great time. If it is not on your “bucket list”, add it now! But the takeaway was this: There were two floats – which cost, from what I can gather, anywhere from $100,000 to $250,000 even though they utilize a lot of volunteer help – from pet rescue groups. They were cute and impressive and, to me, indicate just how much money these people have to throw at positive PR. Add that to the Sea World float surrounded by sheriff’s deputies and policemen in riot gear after a protest from an animal rights group and you have somewhat of a theme that we in the livestock business know all too well. And another issue for 2014 and beyond.

But I firmly believe that happiness is a choice. The Apostle Paul wrote that he was content in any circumstance. Regardless of what 2014 brings, may it be so for you this year!

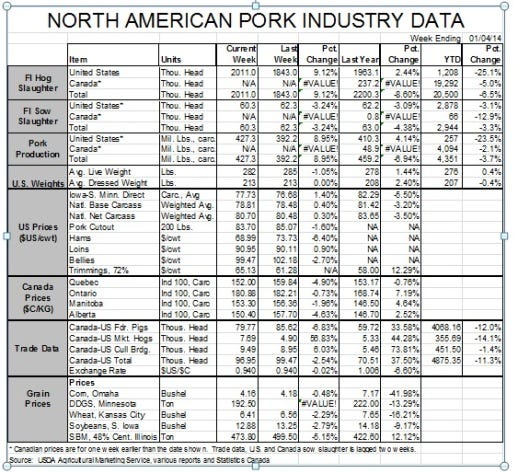

NOTE: Canadian supply and prices in today’s tables represent 12/14 and 12/21.

You might also like:

2014 Looks Good for U.S. Pork Producers

Pace of PEDV Cases on the Rise

You May Also Like

Enter a zip code to see the weather conditions for a different location.