Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

November 11, 2013

First things first. Thank you to all of our readers who have served in our country’s armed forces over the years! While Memorial Day is rightfully a day of thanks and reverence for those who paid the ultimate price for our freedom, Veterans Day offers that tremendous opportunity to personally say “Thank You!” to the veterans who still live and work beside us every day. Take time today to give your dad or uncle or son or daughter a call to tell them you appreciate what they have done or are doing for our great country. Walk down the hall and thank that co-worker who was deployed to Iraq or Afghanistan over the past decade. And especially say thanks to the few remaining of The Greatest Generation and the many remaining who never got proper and much-deserved gratitude when they answered the call to fight an unpopular yet valiant war in Vietnam. Our undying gratitude is due them all!

Was Friday’s World Supply and Demand Estimates (WASDE) report from USDA the nail in the coffin for high grain and feed prices? I guess not if you consider $4/bushel still high for corn or $400/ton still high for bean meal. I would have to agree on the latter of those two but $4/bushel is so far below the past few years’ predominant prices that I have to say that one is a short-term win for sure. The longer term isn’t certain at all but the trend is definitely good.

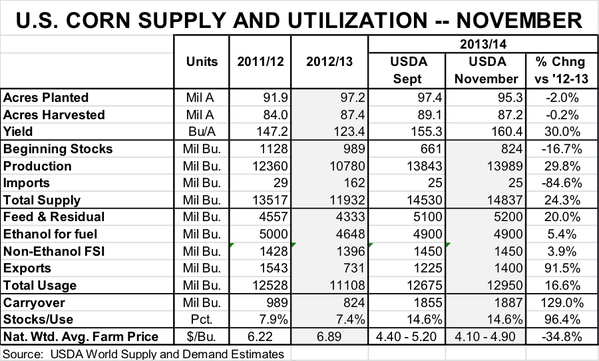

To recap the report, USDA confirmed this year’s record-large corn crop by pegging the national average yield at 160.4 bushels per acre. That near-trend yield is over 5 bushels higher than the September estimate and 27 bushels larger than last year’s average. USDA did, as expected, shave some off its planted and harvested acreage estimates and the reduction was about pne million MORE than had been anticipated by the analysts surveyed before the report. The 2013 crop is still record-large at 13.989 billion bushels, 30% larger than last year.

USDA did increase its estimates of both feed/residual (+100 million bu.) and exports (+175 million bu.) relative to the September report, but even 1.842 billion bushels more of corn usage for this year will still leave 2014 carryout stocks at 1.887 billion bushels. That is 130% more than last year and puts the year-end stocks/use ratio at a relatively comfortable 14.6%.

Like what you’re reading? Subscribe to the National Hog Farmer Weekly Preview newsletter and get the latest news delivered right to your inbox every week!

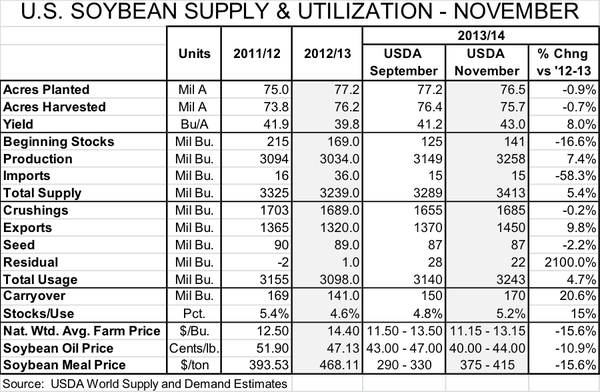

In spite of a larger soybean yield (43 bushels/acre) and the third-largest U.S. crop in history, year-end soybean stocks are still pegged at only 170 million bushels, and the year-end stocks/use ratio for 2014 is estimated to be only 5.2%, the seventh-lowest ever. Thus, the vast difference between historic corn and soybean meal values.

What’s more, the pattern of high prices appears to be at an end for corn and likely ending for soybeans. University of Illinois economists Dr. Scott Irwin and Dr. Darrell Good, found such in their analysis of price runs published last week at their farmdoc website (http://farmdocdaily.illinois.edu/). The above-average runs for both have been historically very long and will not, again judging by history, likely experience another long above-average run soon. But history does not suggest that corn and soybean prices will spend a long period below their 2006-2013 averages of $4.95 and $11.50. Wrote Irwin and Good, “The more likely outcome is a series of positive and negative runs [relative to the averages] of varying but shorter lengths.

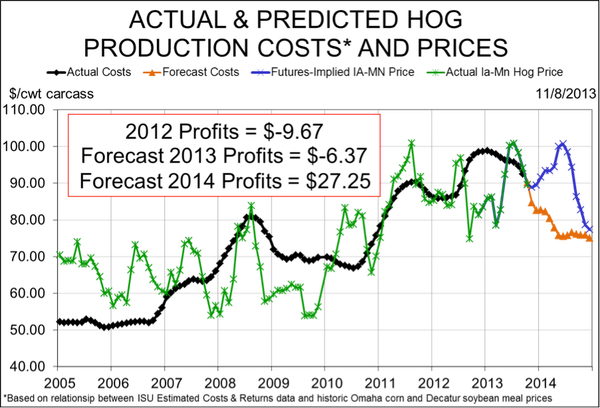

The net impact, though, of the WASDE report is very positive for pork producers. My model puts 2014 projected costs of production at $77.14/cwt. carcass (see Figure 3) as of Monday morning, Nov. 11. That figure, when combined with CME Group Lean Hogs futures as of Monday morning, would put 2014 profits for average Iowa farrow-to-finish operations at $27.25 per head. The best of U.S. producers would be about $5/cwt. carcass below that cost figure and about $10 per head above that profit figure. 2014 is shaping up to be a good year indeed. In fact, those profits would surpass the levels of 2004 and 2005 and make 2014 the best year since 1990.

That assumes, of course, that actual costs and prices turn out to be the same as the prices offered by the futures market as of Monday morning. Or that producers pull the trigger and lock in those costs and prices using futures or options positions. Those margins are more than theoretical. There are traders offering that much money for hogs and asking only that much money for corn and soybean meal today.

There is, however, a significant new source of risk for those producers who otherwise would be willing to hedge in future profits: Production risk. We usually don’t worry much about output risk in the hog business. Even bad occurrences do not usually leave us much below normal production. But porcine epidemic diarrhea (PED) virus is posing the kind of losses over a 3-5-week period that grain farmers encounter when they have a hail storm!

What happens if you have hedged June production at a profit of $50 per head but have no pigs to sell in June? For the first time in recollection, that is a legitimate question. One strategy, of course is to not hedge all of your production. I think most producers follow that anyway, desiring to take some risk for the chance of even higher returns on the marginal animals. But your comfort margin probably has to be larger in the face of PED virus. Perhaps you hedge only 4 of 5, or 3 of 5 unique pig flows in case one goes down. Or reduce the hedge percentage of all sales so you can exit any positions that correspond to a loss period and, if market conditions warrant it, at that point increase coverage for other time periods. Perhaps best, use options. They cost more, but that up-front cost is all there will be – no margin calls and, as long as you use only puts for hogs and only calls for feed ingredients, there is no obligation to deliver anything.

New challenges call for new thinking. What might have been out of the question before should probably at least be considered in light of this new risk.

You May Also Like

Enter a zip code to see the weather conditions for a different location.