Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

November 2, 2015

First today, an important personal item for many North American readers of “Weekly Preview.” Our friend and colleague Glenn Grimes of the University of Missouri was hospitalized last week with what has proven to be colon cancer.

Successful surgery was performed last Wednesday to remove the tumor and Glenn’s doctors believe he will fully recover. Such trauma on even a well-kept 92-year-old body is a trial, so please keep Glenn and his wife, Dorothy, in your prayers. She reported this morning that he is doing well but that this is just going to take a while.

I don’t think Glenn keeps up with email much anymore but I’m sure he and Dorothy would love to hear from you. Their mailing address is 401 Cedar Lane, Columbia, MO 65201. Please drop them a card and, by all means, keep them and their sons in your prayers. Get well soon, Glenn!

♦

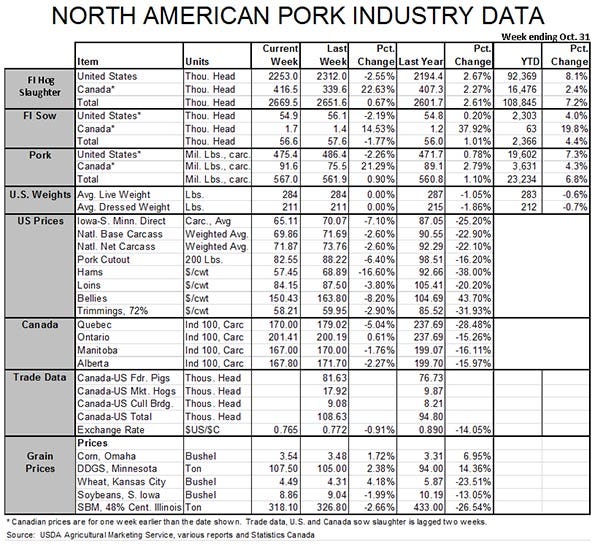

Last week’s decline in the pork cutout, hog prices and ham prices were a bit larger than the normal seasonal drops but we have to remember that they had outperformed the normal seasonal pattern to this point. Hams took the big hit with the ham primal value dropping over $11 to just $57.45 last week, but every other cut was lower as well. The negative forces even got to bellies which had been pretty much bulletproof so far this fall.

If there is a concern in my mind, it is that this decline happened even while weekly slaughter declined from one week earlier. The 2.253 million head in last week’s total was just 2.7% larger than last year, and was a full 5% below my forecast level based on Sept. 1 market hog inventories.

It was a very tough week for Lean Hogs futures with contracts losing $6 to $8. The biggest damage was done to the December contract which fell from $67 on Oct. 20 to just $59.20 on Friday – and is down another $0.88 on Monday afternoon. Those summer contracts that were near $80 are now in the $75 range.

It is likely that the boat has sailed on pricing hogs this fall. It shouldn’t be much of a surprise since “cash is king” and seasonal cash weakness almost always drags the futures complex down at this time of year. This decline is pretty dramatic but not that unexpected – at least to me.

I do not believe there is much reason to panic about next summer however as we still think hogs will be in the upper-$70s. Further, the normal spring rally usually provides better chances for summer pricing.

Consider the bad news that was dumped on this market last week. The World Health Organization’s International Agency for Research on Cancer risk report (which was negative but has been widely panned – and even softened somewhat by WHO itself), Subway’s terribly misguided announcement that it wanted product produced with no antibiotics and a Cold Storage report that said stocks were large indeed. All of those were pretty certain to leave a mark on a futures market that is, even on a good day, very emotional. I would not be surprised to see much of this lost ground gained back in a few weeks.

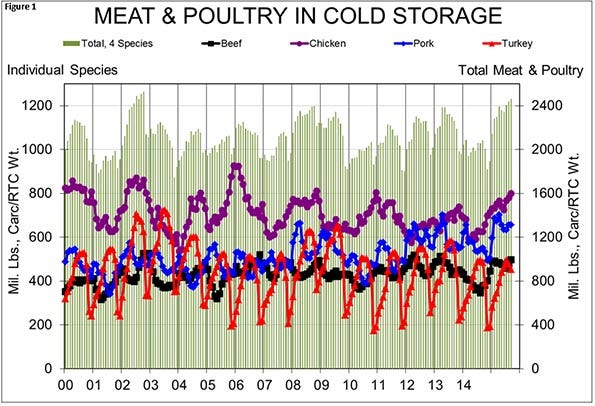

Freezer inventories are indeed a reason for concern. See Figure 1. The total inventory of beef, pork, chicken and turkey on Sept. 30 was 2.461 billion pounds, among the largest ever. A note from the chart that turkey is a much smaller portion of the late-year total than it was back in 2002 when the previous record was established.

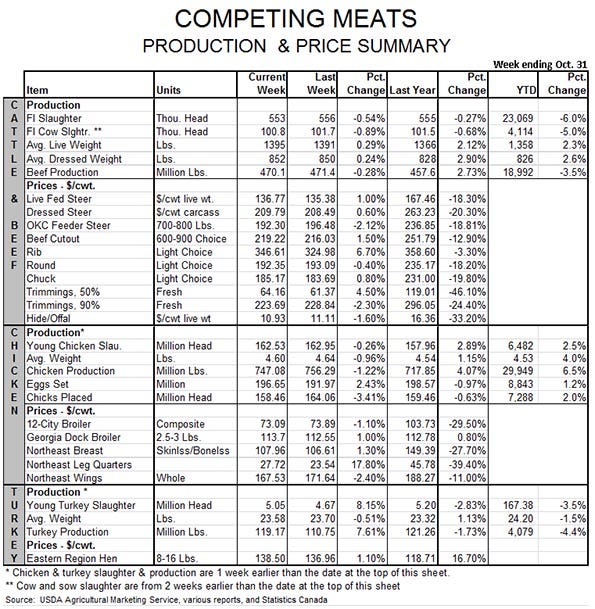

Of the four major species, turkey stocks were the only one that was smaller than last year, falling 6.4% primarily due to last spring and summer’s avian influenza losses. Of the other three species, pork’s plus-19.2% was the smallest year-on-year gain. Frozen chicken stocks were 28% higher and beef stocks, driven largely by higher imports of grinding beef to backfill for lower cow slaughter, were up 31% for 2014.

With beef production getting back to year-ago levels due to huge slaughter weights and rising pork and chicken output, these stocks will hang over the market for a while and likely blunt any big rallies that may otherwise take shape.

You May Also Like

Enter a zip code to see the weather conditions for a different location.