Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

June 29, 2015

The USDA’s quarterly Hogs and Pigs report, released on Friday, will likely be neutral for cash and nearby futures contracts and slightly bullish for deferred futures.

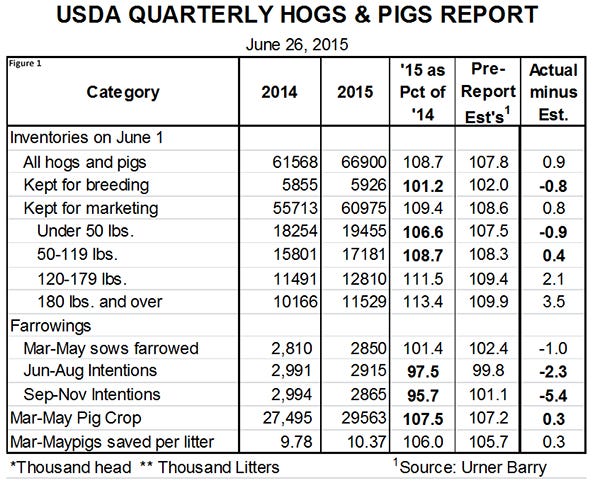

The report’s key numbers were a mixed bag with some inventory figures quite close to analysts’ pre-report expectations (which I interpret as information that was “in the market” at the time the report was released) and others differing pretty markedly. The key data from the report appear in Figure 1.

The market herd was pegged at 60.975 million head, 9.4% larger than last year. Analysts were expecting, on average, an 8.6% increase in the market herd. The key here, though, is the dramatic differences in the numbers and year-on-year changes in the various weight classes.

The inventory of pigs weighing 180 pounds and more was estimated to be 11.529 million head, 13.4% higher than one year ago. That number is well above what analysts were expecting and is likely a bit high given that slaughter since June 1 has exceeded year-ago levels by 10.8%. With today’s market weights, there are still some of these pigs left in inventory but we doubt that slaughter the next two to three weeks will exceed last year’s totals by enough to close that gap much.

The 120-to-179 pound inventory was significantly larger than expected as well, with the 12.81 million head representing an 11.5% gain on 2014. That figure is 2.1% higher than analysts expected, implying that these large year-on-year slaughter gains will persist through August.

The lighter weight inventories were about as expected with the under-50 pound class being almost 1% smaller than analysts had estimated. The 6.6% gain in this category is a bit smaller than the 7.5% year-on-year increase in the March-to-May pig crop. The difference between those numbers is, in my opinion, right on the cusp of indicating some inconsistency in the report but not enough to cause me much concern.

Perhaps the biggest surprise in the report was the 1.2% increase in the breeding herd. That figure is below the lowest pre-report estimate from market analysts and is well below the 2.0% average of analysts’ estimates. It definitely does not fit with anecdotal evidence of robust sow farm construction, but will likely be viewed by the market as a supportive factor for 2016 futures contracts.

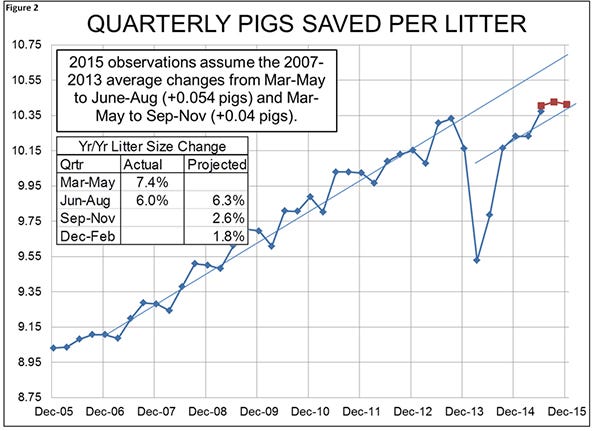

The report confirmed that litter size growth is back on track. The March-to-May average for pigs saved per litter of 10.37 was a new record high and 6% higher than last year’s number that was still being negatively impacted by porcine epidemic diarrhea virus losses. As can be seen in Figure 2, this past quarter’s actual USDA estimates are very close to the 10.40 pigs per litter that I had computed back in April as a likely litter size given the December-to-February figure and normal seasonal patterns from 2007 through 2013. That same computation method would put litter sizes in June-to-August and September-to-November at 10.43 and 10.41, respectively. I have put a line with the same slope as the 2007-13 trend on recent litter sizes and it is obvious that the industry has to potential to be increasing productivity growth rates. The next two quarters’ forecasts imply gains of 2.6% and 1.8% versus last year. A resurgence for PEDV could derail these gains but until we see evidence that PEDV is back, I’m going with a litter size growth rate of 2%.

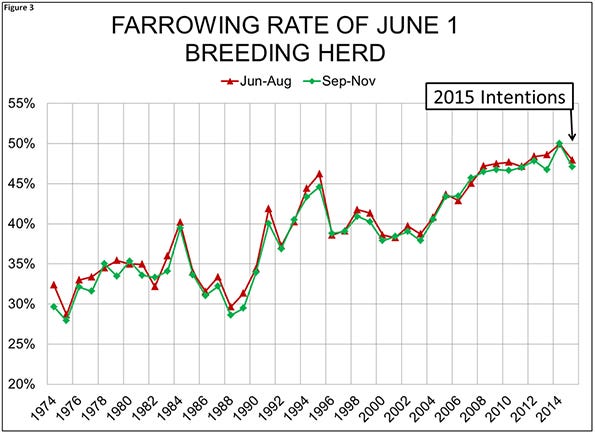

The oddest numbers in the report are for farrowing intentions the next two quarters. Analysts are declaring that they cannot be correct given a 1.2% larger sow herd and, if that was all there was to the story, I would agree. But it is not. As with everything this year, we must be careful comparing to 2014 numbers. Figure 3 shows the farrowing rates of the June 1 breeding herd in the subsequent two quarters. As was the case for the March 1 breeding herd, the screwy numbers in terms of farrowing rates are not the ones in this report. They are the ones in last year’s report. If one adjusts last year’s farrowing rates for the June 1 breeding herd to the average of 2008 through 2013, last year’s farrowings would have been 2.859 million litters in June-to-August and 2.809 million litters in September-to-November. This year’s intentions of 2.915 million litters and 2.865 million litters in the respective quarters would both be 2% larger than one year ago – a figure that is hardly out of line with a 1.2% larger breeding herd. My conclusion: Use the USDA intentions numbers.

The combination of litter sizes and farrowings discussed above would put the June-to-August pig crop unchanged from last year and the September-to-November pig crop down 2% from last year’s level.

At this point, we expect weights to take about 2% off of production the rest of 2015 and to be close to year-ago levels in 2016 given potentially lower feed prices.

Deferred futures have indeed rallied in early day trading on June 29 but I still believe the futures have been significantly oversold during June and that there is some top side remaining. I believe national net negotiated prices will average $73 to $77 per hundredweight carcass in the third quarter and $64 to $68 per hundredweight in the fourth quarter. That third quarter price will be profitable while the fourth quarter forecast implies losses of $10 to $14 per head for average producers. The best producers will be right around breakeven for the fourth quarter.

Deferred futures have indeed rallied in early day trading on June 29 but I still believe the futures have been significantly oversold during June and that there is some top side remaining. I believe national net negotiated prices will average $73 to $77 per hundredweight carcass in the third quarter and $64 to $68 per hundredweight in the fourth quarter. That third quarter price will be profitable while the fourth quarter forecast implies losses of $10 to $14 per head for average producers. The best producers will be right around breakeven for the fourth quarter. Next year looks slightly better in terms of hog prices, but the key issues remain breeding herd growth and PEDV. Is growth really as small and slow as the USDA says? Have producers and veterinarians learned enough to battle PEDV to a standstill in 2015-16?

Next year looks slightly better in terms of hog prices, but the key issues remain breeding herd growth and PEDV. Is growth really as small and slow as the USDA says? Have producers and veterinarians learned enough to battle PEDV to a standstill in 2015-16?

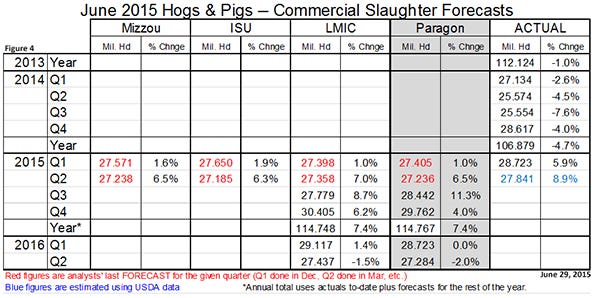

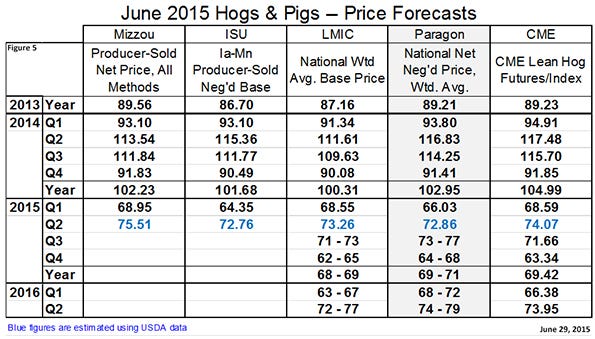

Figures 4 and 5 show my forecasts for quarterly commercial slaughter and prices, as well as those of the Livestock Marketing Information Center. A completed version of the tables will be included in next week’s “Weekly Preview” newsletter.

You May Also Like

Current Conditions for

51°F

Mostly Sunny

Day 72º

Night 50º

Enter a zip code to see the weather conditions for a different location.