Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

Circle Aug. 10 on your calendar. That is the day USDA will release its monthly Crop Production and World Agricultural Supply and Demand Estimates (WASDE). It may also be the single most important day for U.S. livestock and poultry producers any of us can remember

July 23, 2012

Circle Aug. 10 on your calendar. That is the day USDA will release its monthly Crop Production and World Agricultural Supply and Demand Estimates (WASDE). It may also be the single most important day for U.S. livestock and poultry producers any of us can remember. Dec. 23, 2003, when bovine spongiform encephalopathy (BSE) was discovered in the United States was a big one, but the impact of the next WASDE report could be even larger.

The August reports are so important because they will be the first to be based on actual yield survey data for 2012. May’s and June’s ill-advised 166 bu./acre yield estimates for corn and even July’s 146 bu./acre yield estimates were based on past trends, with adjustments for time of plantings and crop conditions. The August estimate will be determined by sample plant counts, ear counts, kernel counts, etc., and will provide us with the first direct measure of this year’s yield. Add in some refinements of harvested acres, which may not be a pretty story either, to get this year’s crop estimates.

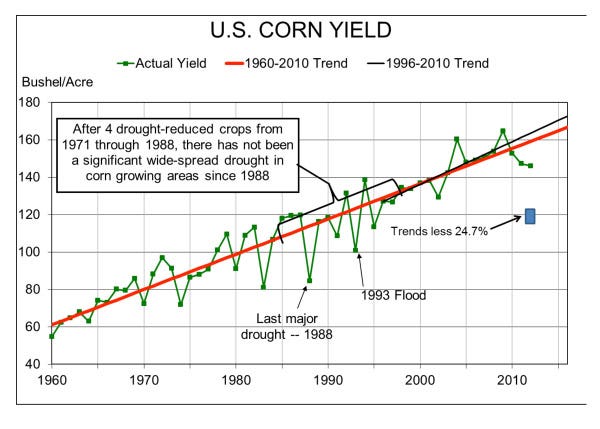

How bad could it be? In 1988, the actual national corn yield fell short of the trend level by 24.7%. Figure 1 shows historical yield, USDA’s current 146 bu./acre estimate and a box that represents the yields that would occur if this year’s yield falls 24.7% below either of the trend lines shown. Only 118 to 121 bu./acre would give us a crop of about 10.5 billion bushels – if harvested acres remain at 88.9 million. That’s unlikely. That crop would put available stocks at just 11.3 billion bushels. The current total usage estimate is 12.72 billion! That usage is obviously predicated on a roughly 13-billion-bushel crop. Much higher prices will prevail if the output is below 11 billion bushels.

The message here is that corn usage will have to decline. Who will blink?

The cost-related challenge for pork producers is the cash (spot) price of weaned pigs. Demand for these amazing little critters is “derived” from expectations of future live hog prices and the cost of transforming the 12-lb. weaned pig into a market hog 5-6 months hence. Neither end of that deal has been good the past few weeks with the feed component, of course, being very, very negative.

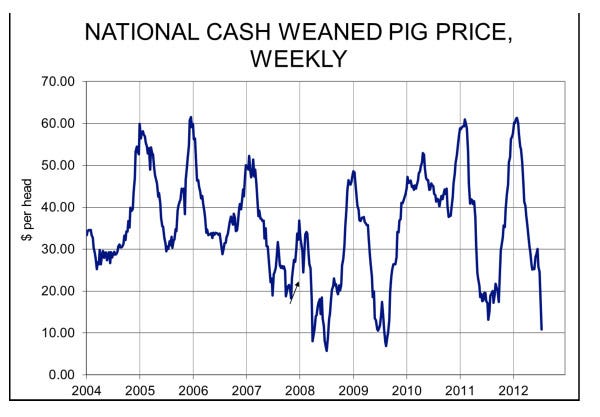

Figure 2 shows weekly weighted average prices back to January 2004, when USDA first began reporting weaned pig prices. Last week’s quote was $10.89/head. We’ve been here before. The 2008 dip to less than $10/head was just like last week – driven by sharply higher feed costs. The summer lows of 2009 were driven by H1N1 and an unexpected larger supply of hogs. Both pushed futures prices lower. Feed was not a bargain in 2009, but it was not the main driver.

Figure 2 shows weekly weighted average prices back to January 2004, when USDA first began reporting weaned pig prices. Last week’s quote was $10.89/head. We’ve been here before. The 2008 dip to less than $10/head was just like last week – driven by sharply higher feed costs. The summer lows of 2009 were driven by H1N1 and an unexpected larger supply of hogs. Both pushed futures prices lower. Feed was not a bargain in 2009, but it was not the main driver.

The concern this year is that we may not get anywhere near the kind of rapid bounce seen in 2008 and 2009. While the market hog price benchmark will move away from the February contract to spring and summer contracts that are usually higher, these feed prices may have a long, long impact. Iowa State University estimates that it costs about $42 to produce a weaned pig. That number is likely to move higher as sow herds consume more of today’s more expensive feed ingredients. It will take a dramatic recovery to move these pigs back into a profitable range, very likely more than pig finishers are willing to pay.

Cold Storage – Good News, bad News

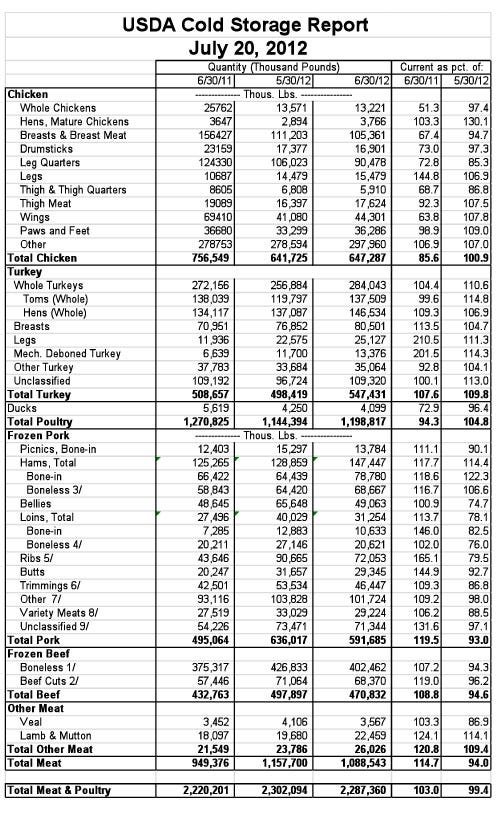

USDA released its monthly Cold Storage report on Friday (Figure 3) and it was a good new-bad news situation for pork. The good news was that freezer stocks on June 30 were 7% lower than one month earlier. I had expected this number to be lower based on the cutout and hog value rally in June.

The bad news was that there was still 7.6% more pork in freezers on June 30 vs. one year ago and that the 591.7 million pounds is a record high for June. Every pork cut category showed year-on-year inventory increases. Stocks of hams and ribs grew the most relative to 2011. Stocks of bellies were up only 0.9%, year-on-year, and were down over 25% during the month.

Total frozen meat and poultry stocks remained 3% higher than last year, but were down 0.6% from May.

You May Also Like

Enter a zip code to see the weather conditions for a different location.