Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

February 1, 2016

Hog and pork supplies have been almost precisely as we expected following the release of the USDA’s quarterly Hogs and Pigs Report on Dec. 23.

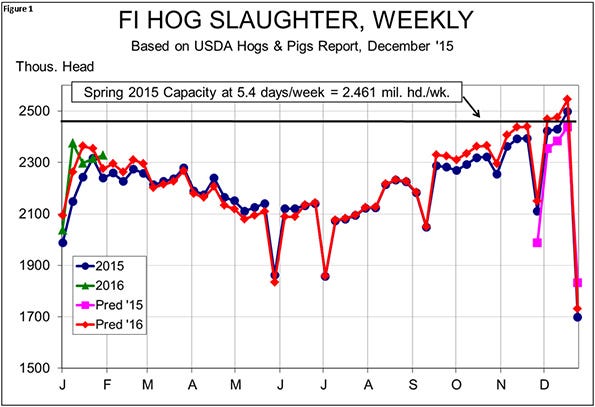

Figure 1 shows our forecast weekly slaughter levels (pink for December 2015 and red for 2016) as well as the actual numbers for all of 2015 and 2016 year-to-date. While there have been some sizable differences between the predicted and actual levels for some individual weeks, total slaughter since Dec. 1 has been only 0.22% larger than our predicted levels.

That miniscule discrepancy says far more about the USDA report than it does our forecasting ability. There is no reason to call the report into question at this time, leaving us confident in our weekly slaughter forecasts — at least for now.

Those forecasts indicate down-trending weekly slaughter totals that are slightly larger than one year ago through February. Our forecast of 1.7% larger first quarter slaughter still looks good. We expect smaller hog numbers (by 1.7%) in the second quarter.

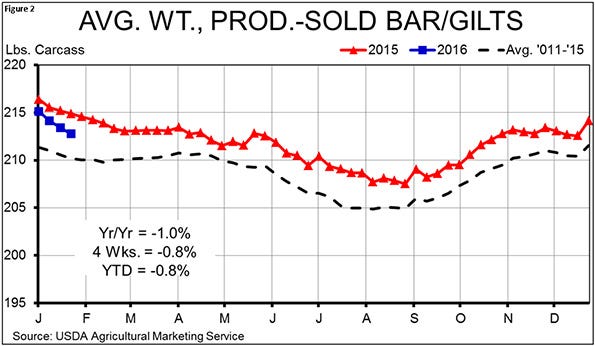

Hog weights have, as expected, remained below year-ago levels so far in 2016. The average weight of all hogs (which includes sows, boars and lightweight hogs) has been down, on average, 0.7% versus 2015. The average weight of barrows and gilts reported under the USDA’s mandatory price reporting system is down a similar amount (0.8%) over the first four weeks of the year, but the year-on-year gap has been growing! See Figure 2.

These animals, which represent the bulk of hog slaughter, averaged 215.1 pounds per carcass the week of Jan. 9. That compares to 216.4 one year ago. Last week those numbers were 212.8 and 214.9. Weights normally fall the first few weeks of the year as plants catch up following holiday-shortened workweeks but this decline is unusually rapid, even compared to last year when hog prices were falling due to problems at West Coast ports. Producers are apparently having to dip a bit deeper into the supplies of pigs in their finishing barns to meet packer demands. It appears the industry is current in their marketing chores on an up-trending market. That suggests stronger cash hogs ahead.

USDA’s monthly Cold Storage report for January indicated that total stocks of beef, pork, chicken and turkey were still burdensome on Dec. 31. The total in freezers on that date was 2.122 billion pounds, 14.4% more than one year ago. Chicken stocks remain near record large at 862.1 million pounds, 2.2% smaller than on Nov. 30, but 21% larger than last year. Chicken inventories have been double-digits larger in percentage terms every month since February. Beef inventories grew marginally in December and remain 15.6% larger than last year.

The frozen pork situation is much better than that of the other large species. Dec. 31 pork stocks were 2.7% lower than on Nov. 30, and were only 8.3% larger than one year ago. That’s the smallest year-on-year increase since February. In addition, the December drawdown in pork inventories was 1.532 million pounds when, on average, pork inventories increase by about 1.5 million pounds in December. Further yet, that decline in stocks was accomplished as production reached the second largest monthly total ever and the largest per day level in history. Stocks of ribs and loins are still large from a historical perspective, but bellies and ham inventories are very near their five-year averages. Ham stocks have fallen from 247 million pounds to just 67.8 million pounds since Sept. 30.

A big question for 2016 hog and pork supplies is the impact that porcine epidemic diarrhea virus might have on pig survival rates this winter. So far the news is good on this front with the number of sow farm breaks being about the same as last winter. The University of Minnesota’s Swine Health Monitoring Project reported breaks at only three sow farms for the week of Jan. 15. Since Nov. 1 there have been 27 sow farms in the U of M sample report PEDV breaks. Just fewer than 20 farms reported PEDV breaks during the same time period last year so the disease is popping up a bit more this year. Veterinarians had speculated that this year might be worse since the number of sows carrying immunities this year would be lower than one year ago because we were one year removed from the huge PEDV epidemic of 2013-14, and the fact that many of the sows exposed during that outbreak have been culled. Producers with roughly 2.5 million sows on about 1,000 farms participate in the U of M system.

November saw a year-on-year increase in the number of sow farms breaking with PEDV but those figures have returned to year-ago levels since. We do point out that PEDV case numbers jumped to nine during two weeks in February last year so we are far from in the clear but at this time, we are making no adjustments to the USDA’s December numbers or our forecasts. PEDV is still a challenge, but it appears to be having no more and no less impact than it did one year ago.

Porcine respiratory and reproductive syndrome has been more active this year than in the past three years. In fact, three of the worst weeks on history have occurred since early December, but there have also been three weeks with three or fewer sow farms breaking. We hear that, while case numbers have declined, PRRS is causing very high death losses. We believe PRRS has likely killed more pigs this winter relative to last year but we doubt that those numbers are significant enough now to adjust our forecasts. This is a situation that merits close attention.

Finally, there is the issue of the great semen extender snafu. Direct information and hard data are hard to come by on this one but there are farms that saw significant litter size reductions beginning in July. Any reduction of pig numbers that occurred should just now be beginning to show up in hog supplies. The important questions are a.) Did producers report pig numbers per those losses in the September and December surveys and b.) Did USDA correctly and accurately include those lower numbers in its pig crop estimates for those two quarters?

As pointed out earlier, pig supplies have been about as expected per the USDA report. If the report’s inventories correctly reflect last summer’s litter size reductions, then our forecasts should be fine. If it didn’t, we may see shorter-than-expected runs soon.

The “expected” slaughter numbers of recent weeks along with falling weights and rising prices suggest that packers are chasing tighter supplies. If that is the case, all three of those patterns will not continue. Slaughter will most likely begin falling behind forecast levels as producers become reticent to sell lighter and lighter pigs.

My “keep your powder dry but ready” admonition remains regarding pricing pigs. Summer futures have traded above $80 with June hitting $81 today. Several contracts are approaching key resistance levels established in September before the fourth-quarter slide. You should be ready to price hogs when it appears this rally has run its course. I’m sure your broker can present several useful strategies to accomplish your pricing goals given the opportunities that are being afforded.

You May Also Like

Enter a zip code to see the weather conditions for a different location.