Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

USDA’s March Hogs and Pigs report implies some big slaughter numbers for this fall.

April 9, 2012

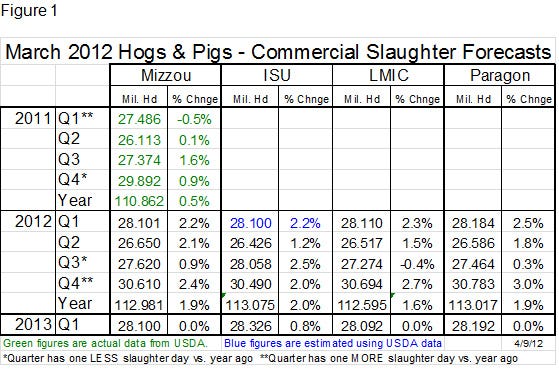

USDA’s March Hogs and Pigs report implies some big slaughter numbers for this fall. Figure 1 shows my slaughter forecasts along with those of agricultural economists Ron Plain at the University of Missouri, Shane Ellis of Iowa State University (ISU), plus the Livestock Marketing Information Center in Denver. The forecasts all translate USDA’s higher inventory numbers into higher slaughter totals through the end of the year, but indicates Q1-2012 slaughter will be relatively steady with Q1-2013.

I have adjusted for the difference in number of slaughter days in Q3 and Q4 2012 vs. 2011. It appears Plain and LMIC have done so as well. The ISU numbers do not appear to be adjusted .

The most noteworthy items in this table are the huge numbers for Q4 and the roughly 2% increase in annual slaughter for this year. Should these forecasts be right, Q4-2012 commercial slaughter will break the previous record high of 30.396 million head set in 2007. And, if the annual projections come to pass, 2012 will rank as the third largest slaughter total in history, trailing only the record 116.452 million head of 2008 and second-best 113.618 million head of 2009.

Do we have enough packing capacity to handle these numbers – especially in the fourth quarter? I believe we do, but barely. My capacity numbers from last spring, adjusted for higher numbers at the Rantoul Foods’ plant in Illinois, indicated that we can slaughter nearly 440,000 hogs per day or 2.376 million head per 5.4-day work week. That number was 2.322 million in the fall of 2007. The 50,000 head/week difference shoud be able to handle this year’s run barring any significant problems.

But I am still very concerned about the fall of 2013, if expansion and productivity gains continue at their current pace. A 0.75% larger sow herd producing 1.5 to 2.0% more pigs per litter adds 2-3% to slaughter by next fall and that number will exceed current capacity levels with little, perhaps no, expansion in sight.

The news from Triumph Foods about their long-expected plans for a second plant in East Moline is not good. It appears that project is delayed indefinitely. I am aware of no other plans for plant expansions though I am trying to verify that for an update in the May issue of National Hog Farmer. Any increase in production by producers will be problematic to say the least.

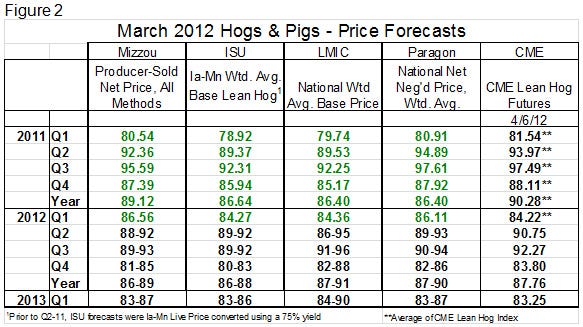

Price Forecasts Adjusted

As for price expectations, analysts lowered their forecasts slightly. Figure 2 shows actual quarterly prices for 2011 and Q1-2012, plus forecasts through Q1-2013. Most summer price forecasts were reduced $2 to $3/cwt., carcass.

I can’t speak for others, but my reductions reflect the generally soft state of pork demand we have seen this far in 2012, as much as they reflect projected growth in hog numbers. Everyone already expected some increases in supplies, but it now appears that the robust demand levels of 2012 may not be duplicated, especially in light of the bad, albeit underserved, meat publicity garnerd by lean, finely textured beef (LFTB) during March.

What does this say for pricing hogs? Futures prices for summer contracts are back within the new forecast ranges. Markets reacted positively to the report with June Lean Hogs gaining over $3 last week and gaining about $0.25/cwt. in trading Monday morning. July hogs are up over $1.00/cwt. from Friday, as of mid-Monday morning, and are well over $4 higher than before the March report was released. The national weighted average negotiated hog base price gained about $3 last week after dropping below $80/cwt. just prior to the report.

Net hog prices have historically gained just over $10/cwt., carcass, from the first week of April to mid-May. If LFTB gets out of the headlines, I expect the rally to be that large (and maybe larger) this year due to the difficulties we encountered in March. A cash rally would carry summer and fall futures higher, but be ready to take action on price breaks if hog and feed ingredient markets are offering positive margins. As much as I want to be optimistic, the risk encounted thus far in 2012 has me as gun-shy as many of you are.

You May Also Like

Enter a zip code to see the weather conditions for a different location.