Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

June 11, 2012

Last week’s World Pork Expo in Des Moines was another rousing success. Crowds were large for both full days of the event on Wednesday and Thursday and were very good for Friday’s half-day. Exhibitors were generally pleased with the number of producers they encountered and were very pleased with producers’ attitudes and actions. It appears that many were in a buying mood.

The general sentiment of those I talked to was disappointment with this spring’s markets and a large dose of apprehension regarding both feed prices and production expansion over the next two years. Both are understandable and, I believe, well-founded even though the prospects for pork producers’ economic well-being over the next two years are about as varied as at any time I can recall.

Beginning with feed costs, farmers said in March that they intended to plant a record 96 million acres of corn. The weather allowed them to start early, raising the real possibility that even more acres could go to corn this year. Corn planting was completed faster than for any crop on record. Emergence has been very good and is near as fast as in any year on record, although there is talk of some replanting (around 10%) in areas that have not received much rainfall since the crop was put in the ground. USDA included a projected record yield of 166 bu./acre in its April World Supply and Demand Estimates, setting the bar very high for the 2012 crop.

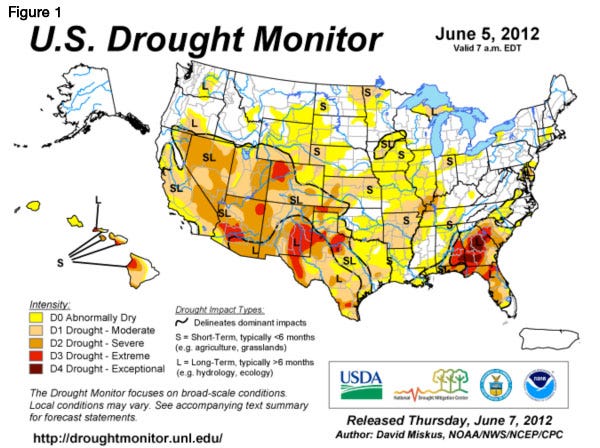

All of that is good and well, but the key now will be actually getting a good yield. And that issue has hog producers concerned as many are from areas that, as of last week, are turning dry (Figure 1). The irony is that the areas in northwest Iowa and southwest Minnesota that we were concerned about just six weeks ago have received ample rainfall. It is the rest of the Corn Belt east of Nebraska that now has us worried. Some areas received rain Sunday night and Monday, but it was indeed spotty. Only western Iowa and northeast Kansas saw significant rains of an inch or more. Thunderstorms were moving across Illinois and Missouri on Monday morning, but no word was available on how much rain had fallen when we went to press.

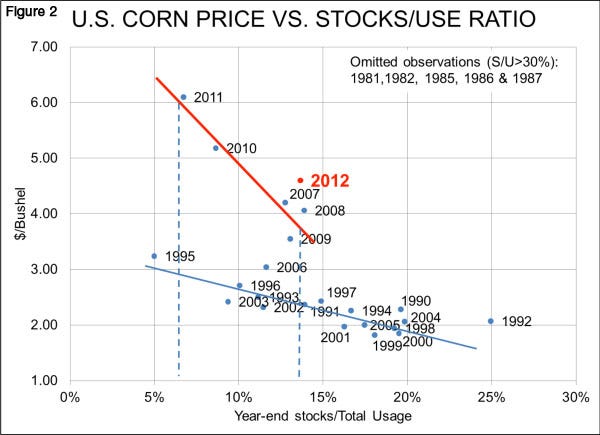

My message to attendees at the World Pork Expo Business Seminar luncheons, sponsored by the National Pork Board, was that prices from $4.00/bu. to $8.00/bu. are still in play for 2012-13 corn. It all depends on rainfall! My wide ranges are based on Figure 2 and the new, much more inelastic relationship we now see between corn supply-to-use ratios and prices.

My message to attendees at the World Pork Expo Business Seminar luncheons, sponsored by the National Pork Board, was that prices from $4.00/bu. to $8.00/bu. are still in play for 2012-13 corn. It all depends on rainfall! My wide ranges are based on Figure 2 and the new, much more inelastic relationship we now see between corn supply-to-use ratios and prices.

USDA’s May supply and demand estimates would leave us with a year-end stocks-to-use ratio of 13.7. Figure 2 says that could give us prices below $4.00/bu. Last year’s yield of 147.9 bu./acre would put the stocks-to-use ratio at 8.5 or so and give us corn prices in the mid-$5.00 range. Should it simply not rain the rest of the summer, yields would likely fall 12 to 15% short of trend (compared to -22 and -25% in 1983 and 1988, respectively) and come in near 136 bu./acre. The various usages would all decline if we had to ration the resulting 12.8 billion bushel crop, but suffice it to say that year-end carryout would fall from this year’s already-tight 851 million bushels. The 2011 record for corn prices would almost certainly be eclipsed.

While the hog market doesn’t look quite this unpredictable, there is still some major concern going forward. I expect hogs to top out this year in the low- to mid-$90s. I still think that will happen in July or early August after we have seen seasonally lower supplies for a few weeks and worked through some of the product that was in the April 30 near-record stockpile of frozen pork.

While the hog market doesn’t look quite this unpredictable, there is still some major concern going forward. I expect hogs to top out this year in the low- to mid-$90s. I still think that will happen in July or early August after we have seen seasonally lower supplies for a few weeks and worked through some of the product that was in the April 30 near-record stockpile of frozen pork.

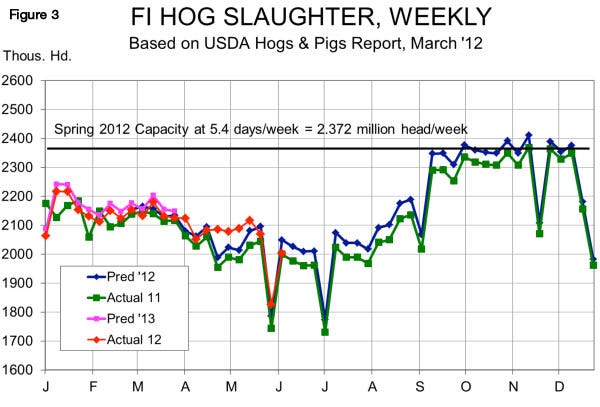

Negotiated hogs hit the low $90s (carcass) last week and the question is now, “Have we seen the highs?” I don’t think so, but some disagreed and I can understand why. The real question is whether the slaughter over-runs that we saw in April and May (Figure 3) return. Two of the last three weeks have seen hog numbers below the expected levels and the anecdotal evidence from Expo is that this will continue for a few more weeks. Past that, the question is whether the +2.5% year-on-year we have for July through September is enough to cover the actual numbers.

And that brings us to expansion. I heard everything from 60,000 sows to 200,000 sows as potential growth over the next two years. The herd grew by 0.55%, year-on-year, for the four quarters that ended March 1, adding 32,000 sows. A continuation of that pace would put the herd at 5.835 million on Dec. 1. That number is also 32,000 head higher than one year earlier. That pace would get us to the +60,000 sows by the end of 2013.

And that brings us to expansion. I heard everything from 60,000 sows to 200,000 sows as potential growth over the next two years. The herd grew by 0.55%, year-on-year, for the four quarters that ended March 1, adding 32,000 sows. A continuation of that pace would put the herd at 5.835 million on Dec. 1. That number is also 32,000 head higher than one year earlier. That pace would get us to the +60,000 sows by the end of 2013.

But adding up Cargill’s Texas expansion with some known expansions of several midwestern systems can, I think, get us a herd that is roughly 100,000 sows larger by December 2013 than it was in December 2011. That would be a 1.7% increase over two years or 0.85% per year. Add on 1.8% per year for litter size growth and 0.5 to 1.0% for higher average weights and you get to +3 to +3.5% per year on pork supplies.

You May Also Like

Current Conditions for

51°F

Mostly Sunny

Day 72º

Night 50º

Enter a zip code to see the weather conditions for a different location.