Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

Examining the accuracy of the June quarterly report

September 7, 2015

So how are hog supplies relative to expectations? That is always a good question to keep tabs on as it has a number of implications for markets both current and future. For the most part, our expectations of hog supplies are based on USDA’s quarterly Hogs and Pigs reports, the most recent of which has proven to be relatively accurate.

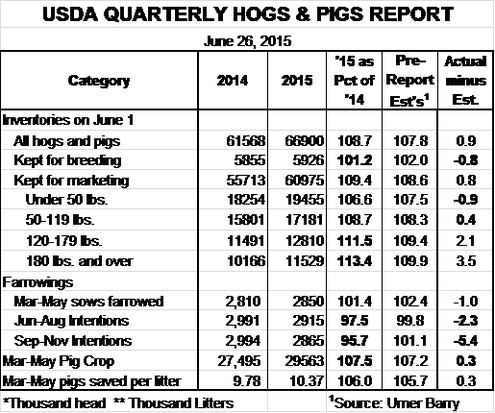

June’s Hogs and Pigs report was short-term bearish and longer-term bullish. See Figure 1 below for a reminder of the June data. The market inventories were expected to be much larger than one year ago in light of lower porcine epidemic diarrhea virus losses last winter but the heavyweight inventories were considerably larger even than the average of analysts’ pre-report estimates. Inventories of lighter pigs were about as expected and suggested a closing of the year-on-year slaughter increase gap as we began to compare this year’s numbers to year-ago numbers that reflect some degree of recovery from the PEDV onslaught. The better disease conditions in 2015 – porcine reproductive and respiratory syndrome 174 notwithstanding – also showed up in a record-large average for pigs saved per litter at 10.37, 6% larger than one year ago. That figure was pretty close to the 5.7% growth rate expected, on average, by analysts.

Figure 1

On the bullish side, most observers were surprised by the modest 1.2% growth rate of the sow herd and were astonished that farrowings in the June-to-August and September-to-November quarters could be 2.5% and 4.3% lower than last year.

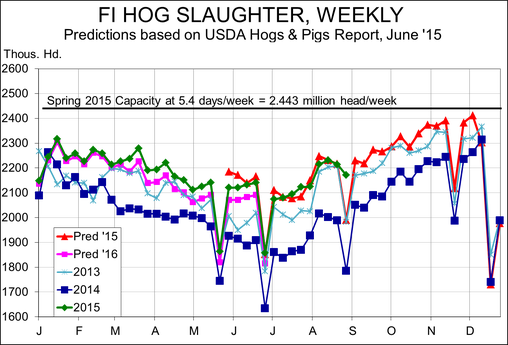

All we know so far is the relationship of slaughter since June 1 versus the market hog inventories. Figure 2 shows those numbers graphically and you can see that they have been similar in most weeks. In fact, the only significant differences between actual numbers (the green line) and our forecast numbers (the red line) occurred the first two weeks in June. Last week’s difference is attributable to an early 2014 Labor Day and a “latest-it-can-be” 2015 Labor Day. From June 1 through Aug. 29, actual slaughter has trailed predicted slaughter by 0.7%. Throw out those first two weeks of June and actual slaughter has exceeded predicted slaughter by 0.3%. Both misses are less than 1%, leading me to be comfortable with the June report.

Figure 2

First, the accuracy of those heavy-weight categories in the market hog inventory and the internal consistency of the June 1 breeding herd, March-May farrowings, March-May pigs saved per litter and March-May pig crop leave me pretty comfortable with our weekly slaughter forecasts for September through November. We’ll get a fresh read on those numbers in the heavy-weight categories of the next Hogs and Pigs report on Sept. 25.

I am still comfortable ignoring the year-on-year percentage change figures for June-to-August and September-to-November farrowings (-2.5% and -4.3%, respectively) and using the actual farrowings numbers based on my conclusion that the 2014 farrowings figures for those two quarters were inflated by PEDV-related disruptions to production flows. The continuing (and expected) absence of PEDV cases on sow farms tells me that litter sizes should be slightly larger than March-to-May’s 10.37. Again, we haven’t seen any flaws in the June report to refute any of that and they imply December ’15 through May ’16 slaughter being 1% lower than one year before. All of those figures, of course are subject to revision when the USDA updates the data in a few weeks.

Similar slaughter to last year should mean similar prices in the first half of ’16, right? I hope not! This year’s first-half prices were impacted severely by the port slowdown and producers’ aggressive efforts to get hogs moved in the face of falling prices. Reducing market weights and making room for what was, for many, a surprising number of surviving piglets also contributed to the rapid rise in slaughter levels and pressure on prices. At present we see no reason to expect any of those factors to repeat themselves this winter.

The four contracts covering the first half of 2016 (February, April, May and June) averaged $73.88 at the close on Friday. The average for the CME Lean Hog Index for that same period in 2015 was $67.82. My first half forecasts would be $71-$75 for national weighted average net negotiated hogs. A decent percentage (50% perhaps) of first half 2016 sales is warranted at these price levels. I wouldn’t argue with higher levels of coverage if you are not comfortable with price risk or if your balance sheet tells you and/or your banker that you should not be comfortable with price risk. Using put options will obviously leave the top side open for you and combination strategies, as always, can get that position established at little or, perhaps, no cost. At the least, you and your broker should have action plans for a bullish report on Sept. 25.

Let’s hope that report is as accurate as the June report has been thus far.

You May Also Like

Current Conditions for

70°F

Partly Sunny

Day 72º

Night 50º

Enter a zip code to see the weather conditions for a different location.