Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

U.S. hog farmers have had some outstanding profitability years. However, this year promises to be a challenging market year with more hogs in the pipeline. Steve Meyer, vice president of pork analysis for Express Markets Inc., explains what is happening with the livestock and poultry industries, and shares these valuable factors to consider while sifting through the ugly market year ahead.

1. Macro conditions continue positive trend

Despite what is going on in the stock market right now, the U.S. economy is still on solid ground, Meyer says. He reminds pork producers at the Iowa Pork Congress that, “The stock market has predicted five of the last two recessions.”

Looking at the U.S. unemployment rate, it remains at a firm number for long-term at 5%, Meyer notes. In addition, real gross domestic product growth has stayed above 2% over the last several years. As for employment, the December figures showed 265 million more people employed at the end of 2015.

Oil below $30 a barrel is great news for hog farmers and leaves a lot more cash in your pockets, says Meyers. Low energy prices reduce the cost of goods for agriculture but also for many business sectors globally. Higher interest rates were also inched higher, which was widely criticized. Meyer says this is part of a long-term strategic plan to provide leverage on the economy for the future.

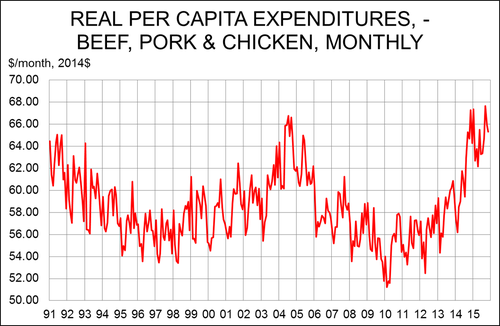

One important macro condition is consumer confidence. Overall, meat and poultry demand has been on a good run for four years. Examining real per capita expenditures for beef, pork and chicken (refer to the chart) to measure the strength of demand, the RPCE year-to-date is up 5.7% as a result of consumers’ willingness to pay for product despite record retail prices. The question is can we hold the gains in meat and poultry demand going forward, Meyer states.

2. Competitive animal proteins

The hog market is heavily influenced by the other species — beef and poultry — in the last several years and this will continue in the future.

Currently, the beef market has been driven by the cow-calf sector with a forecast return of $200 per head in 2016, especially with improved grazing conditions. The profit incentive has motivated ranchers to retain heifers, keeping heifer slaughter numbers lower. As a result, feedlots were sending record heavy animals to market because it was cheaper to feed the animals owned than to purchase expensive replacement feeders. This fall the market dramatically dropped, correcting itself. Meyer says cattle prices will mainly be sideways all year with a forecasted choice cut-out value at an average of $200 per cwt. (Southern Plains), fats in $130 per cwt., feeder cattle weighing 700-800 lbs. $155-$165 and calves weighing in the 500-lb. range near $200 per cwt. Based on his calculation, Meyers estimates beef production will gain 2% in 2016 and grow another 4% in 2017.

On the poultry side, the broiler hatcher flock grew sharply (3%) in 2015. Meyer says this sector is getting close to running at full capacity and new operations will have to go online in order to grow further. In 2015, broiler production was up 4%. Growth for broiler production should be slower over the next two years, especially as producers keep weights at more normal levels. Meyer predicts broiler production to increase 1.2% in 2016 and 1.6% in 2017. Slower broiler production is good news for the hog industry as broiler prices should rise.

For turkey, a new strain of high-pathogenic avian influenza of North American origin was diagnosed in January in a flock of turkeys in Indiana. It appears at this point that there was only one case of HPAI and to date no new cases. As a result, countries only banned poultry exports from Indiana which should not have a ripple effect on the global market. Meyer says there are no indications that HPAI will negatively affect production or exports this year. He estimates 4.7% growth in turkey production this year.

3. Export markets meet headwinds

A strong U.S. dollar will be a continuing factor for the export market. Once the new high of 100.6 for the U.S. dollar was reached in early December, the U.S. dollar has remained strong and is stabilizing. For the most, key players in the export market are adjusting to the “new high” of the U.S. dollar. Overall, U.S. pork exports is weathering the storm well. As result of steady climb, U.S. pork saw positive growth in November with 1.1% year-to-date growth. A robust growth will not be seen at least until the Trans-Pacific Partnership starts taking hold. Meyers says a victory for the year can be called if U.S. pork exports grow 5% this year.

4. Lowest hog production costs since 2007

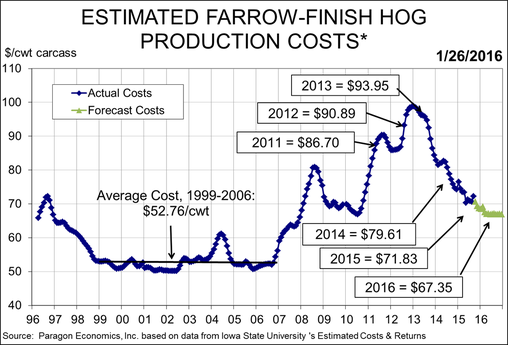

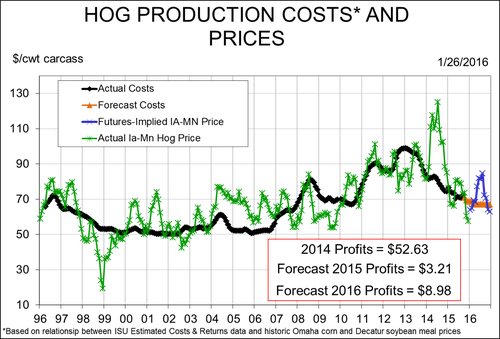

We are back into a different cost environment that is going to be with us for a while, says Meyer. Grain prices are the key to the lowest input costs for hog farmers since 2007. World grain stocks have been restored to more comfortable levels with countries on the average storing 50 million metric tons more grain than in 2012. Assuming a normal crop in 2016-17, corn and soybean prices should remain affordable. According to Meyer’s forecast, the estimated farrow-finish hog production costs should be on the average of $67 per cwt. carcass with best producers’ costs at $61-$63 per cwt (refer to the chart below).

“When you compare that cost to where the future markets are now, this is not going to be a bad year,” says Meyers. “You have an opportunity to make it a pretty good year.”

5. Pork production on the rise

Although some breaks of porcine epidemic diarrhea virus cases have occurred this year, the outbreaks have stayed at low levels so far. At this point, there is no reason to adjust pork production, Meyer says.

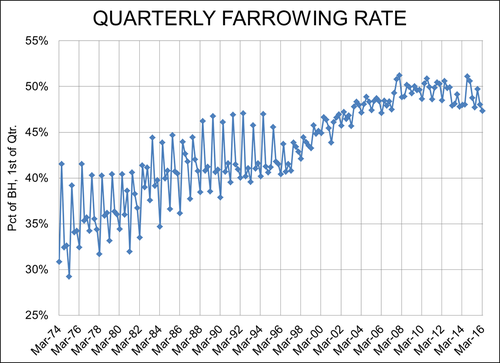

Based on the December USDA “Hogs and Pigs” Report, the hog inventory was a fresh new high at 68 million head. The breeding herd at 6 million head was the largest in over a decade. In addition, the record pigs saved per litter illustrates litter sizes are back on the growth chart. As a repeated pattern for the last two years, the farrowing intentions have been smaller in relative to the breeding herd (refer to the chart below), which is puzzling to market watchers. Meyer says predicting the U.S. hog herd is better based on productivity rather than the size of the breeding herd.

6. Best hog prices in the third quarter

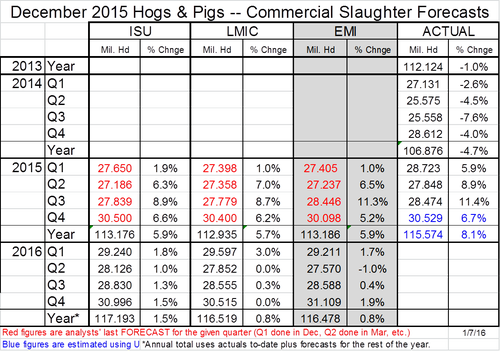

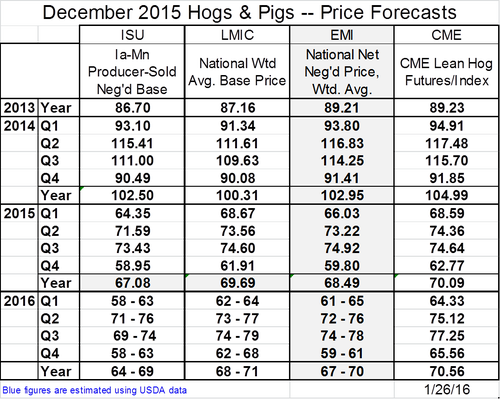

For 2016, Meyer forecasts 0.8% growth in slaughter for the year with a record number in the last quarter (see table).

For prices, he predicts an average $67-70 per cwt. with the lowest prices in the final quarter of 2016 (see table).

Meyer says you have some pricing opportunities right now on the future markets, especially for fourth quarter 2016.

Packer margins were excellent last fall. Keep in mind, moving forward there is going to be a large spread between cut-out value and the value of live hogs — a factor that hog farmers need to keep in mind when negotiating contracts influenced by cut-out values.

7. Narrow profit margins

Combining the previous mentioned fundamentals with the lower cost input, Meyer forecasts 2016 average profits for hog farms at $8.98 per hog. Using the future markets, the year can be profitable but the fourth quarter will be the toughest to market, Meyer concludes.

8. Pay attention to risk factors

The No. 1 risk is a major export disruption. With over 22% of U.S. pork exported, any major export interruption would be a pricing disaster for the U.S. hog market. PEDV is always a risk however the risk is diminishing as the winter months progress. A strong three years of demand was great but slower demand is expected. Domestically, pork demand looks upbeat with an emphasis on proteins in the diets. Globally, U.S. pork exports will face headwinds with a sluggish world economy and a strong dollar. Imports from Canada have increased slightly because of closure of a processing plant rather the end of mandatory country-of-origin labeling. Meyer says this is an item that needs to be watched closely in 2016.

You May Also Like

Enter a zip code to see the weather conditions for a different location.