Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

April 16, 2012

Was last week the first step in running completely out of market hogs this summer? That is a bit too much hyperbole, I know, but I always engage producers and analysts in the “PRRS-has-killed-millions-of-pigs-there-can’t-be-many-left” discussions every year. This year those discussions – and they are discussions, not arguments – have been intense at times.

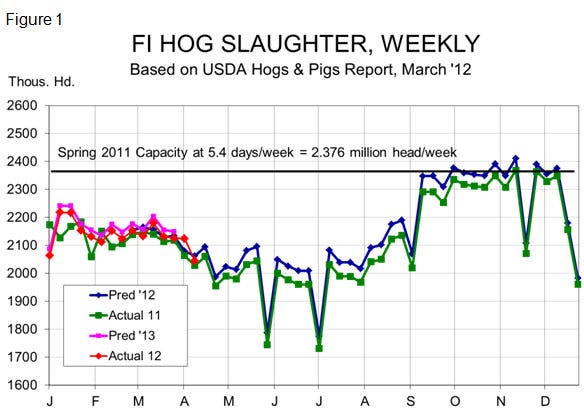

I know it’s a pain but, again, let’s look at the facts. The best facts we have at this time are USDA’s pig inventory and production numbers. Figure 1 shows weekly slaughter for last year, this year (to date) and forecast weekly slaughter from the March Hogs & Pigs report. First, note that slaughter levels have been very close to predicted levels, running just 1% higher since Jan. 1. That means the December and March reports have proven to be pretty close in their estimates of market hog inventories.

Last week’s sharp decline of 80,000 head from the week before was not the first sign of short supplies. It was driven mainly by a short Monday slaughter when some plants were shut down for the Easter holidays. Easter was two weeks later last year, so compare last week to the 104,000-head decline last year, two weeks forward, to directly compare the impact of these Easter slowdowns. This may be an early seasonal down week, but I don’t think it is any more than that.

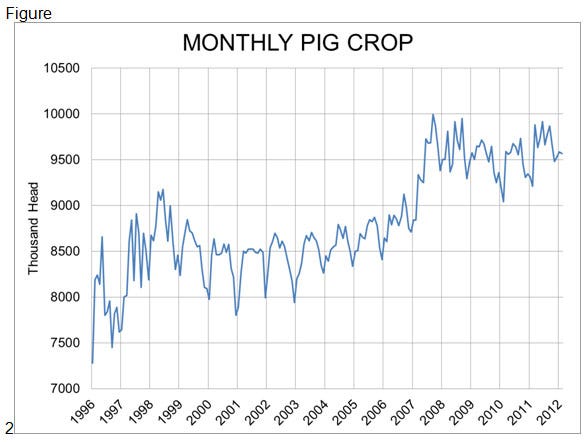

Monthly Pig Crop Trends

Figure 2 (Monthly Pig Crop) shows some data that I should pay more attention to, according to an industry number cruncher that I hold in very high regard. He thinks they show much lower numbers ahead. So I did take a closer look and I have to respectfully disagree.

When you compare the monthly pig crops for this winter to those of the past two years, it appears that we have gotten along better, if anything. November’s crop of 9.482 million head represented a drop of 387,000 from September. That same period saw declines of 398,000 head in 2009 and 429,000 in 2010. Further, the pig crop increased from November to December and December to January this year before falling slightly in February. The pig crops during the previous two years continued to fall into February.

While numbers will no doubt get tighter this summer, I will still stick with the normal annual pattern and the predicted year-on-year changes shown in Figure 1 until proven wrong. The chances are that if I am indeed wrong and porcine reproductive and respiratory syndrome (PRRS) has caused much higher mortalities this year than in the past, numbers will be lower and prices will be higher.

I am not recommending futures or options sales now, anyway, due to the normal tendency of cash and futures prices to rise for the next four weeks or so. Last Thursday’s big rally was encouraging in that regard. And, it agreed with my biases. Friday’s limit down? Not so much. Ditto for today’s ongoing selloff. It’s enough to make me think about throwing in the towel.

The supply fundamentals are not that bad, however. The question is about demand – domestic and international – but we only have data to gauge both of those demand situations through February. March was the month that we all got LFTB’d (lean finely textured beef), I will not say pink s----d, and markets have certainly not recovered yet. Will they recover in time to support a summer rally? I think so. But I don’t think the rally will reach the upper $90s or, as I once thought, touch $100.

If demand returns to more normal levels, expect price strength as hog numbers tighten. If not, the supply numbers may not matter much and we will all be disappointed.

You May Also Like

Enter a zip code to see the weather conditions for a different location.