Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

May 19, 2014

Last week’s slaughter total fell short of 2 million head once again – but just barely. That total is, in fact, large enough to be causing some questions regarding the impact of porcine epidemic diarrhea virus (PEDV). Slaughter numbers since the week ending May 2 have been within 4% of one year ago, and last week’s 1.999 million-head total was only 1.9% lower than last year. The slaughter runs for that period would be comprised primarily of pigs born from late November through the first half of December. And the year of their birth is still 2013 in spite of the fact that their average size suggests some may, in fact, be yearlings! Or old enough to vote!

So have we all been too alarmed about PEDV? I guess that is possible, and some may consider me the chief alarmist, but let’s look at everything that has gone on in the past few months to see if any judgment can be reasonably made at this point.

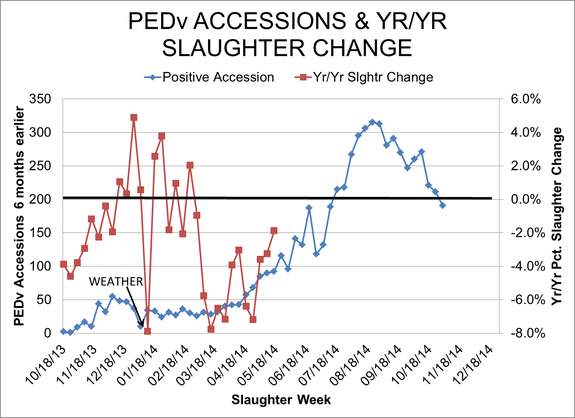

Figure 1 shows the year-on-year percentage change in federally-inspected (FI) hog slaughter (right axis) and the National Animal Health Laboratory Network’s (NAHLN) weekly PEDV case accession numbers from 26 weeks earlier (values on the left axis). So, last week’s year-on-year slaughter total was 1.9% lower than one year ago, and its corresponding 92 case accessions occurred in the week that ended November 16.

Figure 1

It is clear that the relationship so far is anything but tight. Slaughter plunged compared to year-earlier levels for the first week in March. That week corresponded to births from the first week in September when PEDV case accessions were sort of bouncing along in the range of 25 to 35 each week. Conversely, case accessions broke above 50 and started their fall increase during the week of October 19, almost 6 weeks later than one would have expected the pigs from the first very short-slaughter week to have been born – on average.

Further, the year-on-year slaughter changes have been getting smaller. Last week’s figure was the smallest year-on-year decline since the very last week of February--even though the case accessions were climbing steadily for these pigs’ normal birth period in November. What gives?

First, it is possible that the case accession data have misled us (or at least me!) to expect larger losses than have actually occurred. Our ongoing discussion of not knowing much about source farms for the PEDV samples, possible duplications, etc. fits here and still could be true.

But second – and in my mind more important – is the fact that any event that creates an economic incentive also, by its very nature, creates potential solutions to that incentive that can make it appear that the first event may not have happened. I know that sounds like economist gobble-de-gook but . . . okay it is economist gobble-de-gook but it’s still true!

Consider:

Lower hog supplies lit off a price rise that made it profitable to feed pigs to heavier weights.

That action shorted the immediate market of hogs, pushing prices even higher.

The rapid rise in prices drove some end-users to buy product in order to build inventories before prices went yet higher. This buying pushed up cut values and further exaggerated the price increase by pushing packer margins higher.

News coverage of pig losses fueled the buying frenzy by causing fear of shorter numbers this summer.

Producers couldn’t feed the hogs forever, so they finally started making their way to town at the aforementioned large weights. Slaughter has caught up relative to year-earlier levels and supply reductions have gotten smaller, pushing prices lower. Weights have stopped increasing.

But do any of the actions so far actually say anything about the next 4-to-6 months? Maybe plenty, and maybe nothing. Every one of these actions could be written off as fear reactions to misinformation. Or, they can all be explained as very rational reactions to accurate information. The truth is that all have been a mixture of the rational and irrational, in response to data that are neither all bad nor all good. Such is always the case in our business. This is just “normal on steroids” I think.

With all that said, though, we are at a critical juncture. It appears in order for packers to keep slaughter levels just under 2 million hogs per week, they will have to dip deeper into the slaughter supply. And if the vet lab data mean anything at all, that supply should be falling pretty rapidly over the next few weeks, with the impact peaking in August.

I think there will be two key indicator variables. The first, of course, will be prices. Last week, base prices declined by their smallest amount in six weeks, while producer-sold net prices actually gained $0.20/cwt. carcass. Both of those suggest the downward adjustment may be over.

The second indicator variable is slaughter weights. Watch them closely in coming weeks. If big slaughter reductions are coming, I would expect weights to fall at rates slightly faster than the average of the past five years.

Figure 2

Figure 3

You May Also Like

Current Conditions for

51°F

Mostly Sunny

Day 72º

Night 50º

Enter a zip code to see the weather conditions for a different location.