Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

Two months of disappointing hog markets have given way to a healthy rally of pork and hog prices over the past two weeks.

October 8, 2012

Two months of disappointing hog markets have given way to a healthy rally of pork and hog prices over the past two weeks. The rebound isn’t healthy enough to get anywhere near profits, but healthy enough to significantly reduce the losses projected for Q4 hog sales. All along, I thought a rally would come when slaughter numbers returned to more normal levels. Fortunately, for once, I was right in that expectation.

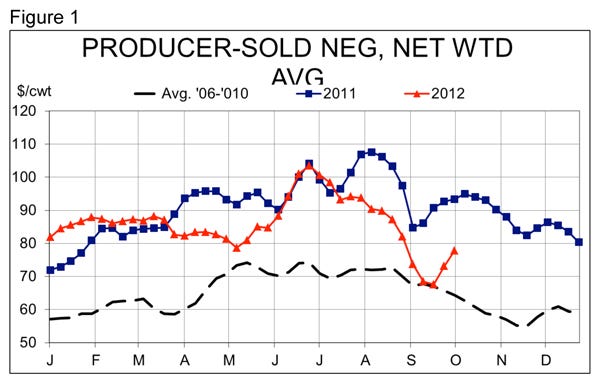

Figure 1 shows the sharp increase in the net price of negotiated pigs sold by producers (i.e., excludes packer-sold pigs). The $10.24/cwt. carcass rally over the past two weeks has offset a good portion of the huge drop in hog prices during August and puts us much closer to a normal seasonal decline. The average decline for early August to early October is about $7.50/cwt. carcass. Even with last week’s gains, this market still stands nearly $16/cwt. carcass below the first week of August. It is very possible that July prices above $90/cwt. carcass had us set up for a larger-than-normal seasonal downturn, so keeping the decline to $7.50 was not likely in the first place.

The rally in hog prices was driven by lower supplies and higher end-use value. The cutout value gained over $6/cwt. the past two weeks. The cutout was driven by improvements in several primal cuts, most notably hams, whose price rose $3 to $3.50/cwt. last week, which put them $11-$12/cwt. higher than they were the beginning of September. Ham prices usually fall during October due in part to the usual increase that occurs as summer hog runs are tight and seasonal demand from ham cookers picks up in July and August. This year was completely the opposite in August and September (Figure 2). I would be surprised to see ham prices move much higher, but steady money through October is a definite possibility at this point.

Loins (+$9), spareribs (+$11) and 72% CL (chemical lean) trimmings (+$12) have also contributed to the recovery in cutout values since Sept. 14.

Abnormal Supply Patterns

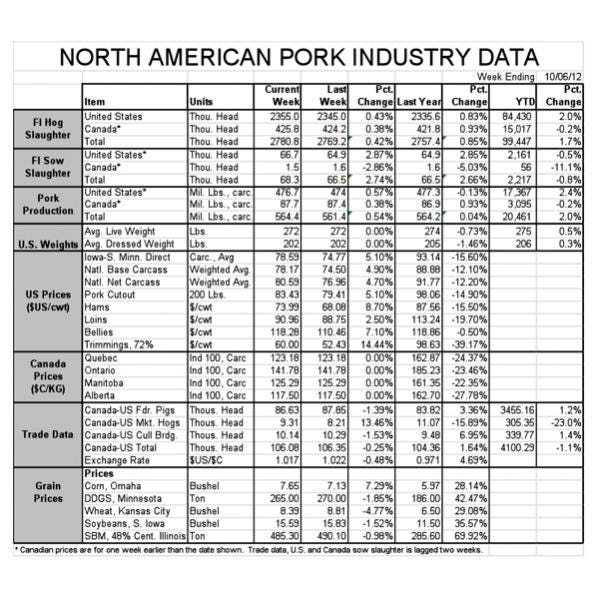

The supply pattern over the past two months has been anything but normal, of course. Last week’s 2.355 million head was right in line with the September Hogs and Pigs Report and is only about 16,000 head higher than the number predicted by the June Hogs and Pigs Report. But slaughter exceeded the June-predicted levels by 718,000 head (3.7%) from the week of Aug. 3 through the week of Sept. 28.

I still think this excess slaughter vs. expectations has put us ultra-current at current market weights. Barrows and gilts reported to USDA under mandatory price reporting weighed 201.8 lb. carcass weight, 0.71 higher than the previous week but 3.3 lb. lower than one year ago. Given Aug. 1 average carcass weights of 200.6 lb., weights should have been 204-205 lb. last week. The 2-3 lb. reduction vs. what “should have been” takes 1 to 2% off of supplies.

Finally, we are now in a time of year that usually sees robust consumer-level demand. Fall supply increases are not normally accompanied by steep retail price reductions even though some of that impact may be masked by the fact that USDA’s retail price data do not pick up feature-priced goods very well.

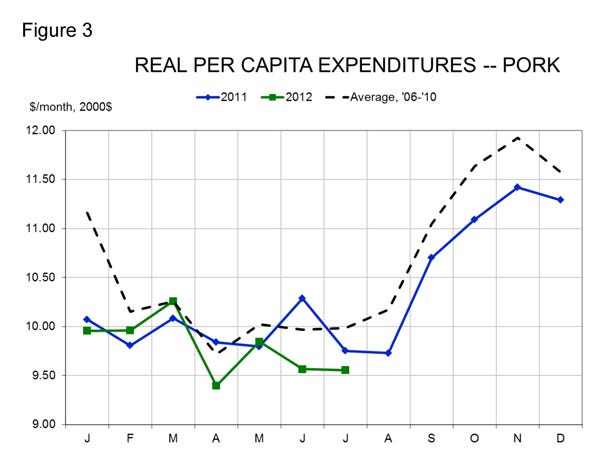

Real per capita expenditures (RPCE; Figure 3) usually rise sharply in September, driven primarily by higher per capita consumption. I think that was precisely the case this year and the response has been higher meat values and hog prices. RPCE usually continues to increase in October through December.

What Lies Ahead?

So what does this mean for pork producers? First, as would be expected, it has carried the nearby October contract back above mid-July levels of $80/cwt. carcass. The contract expires this Friday, though, so the rally will not offer many if any pricing opportunities. It has pulled December from just barely over $70 up to $77 and February and April contracts back comfortably above $80/cwt. carcass. None of those prices are profitable at today’s cost levels, but $6 to $10 improvements mean far smaller losses as was pointed out earlier.

Further, the rally has kept next summer’s futures very near $100 – a price level that could easily prove profitable barring a late-season run on corn if rationing efforts are late in starting. In my mind, any move above $100 would be a pricing opportunity, but don’t get carried away. Beef prices could be very high indeed this coming spring. If that happens, beef could well pull hogs up just as hogs have weighed down other species this fall.

You May Also Like

Current Conditions for

61°F

Mostly Cloudy

Day 72º

Night 50º

Enter a zip code to see the weather conditions for a different location.