Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

October 6, 2014

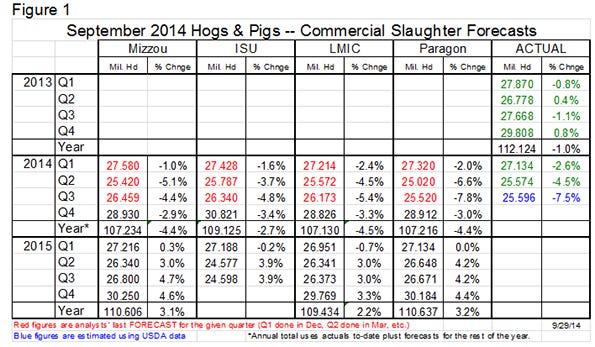

My quarterly post-Hogs and Pigs Report compilations of slaughter and price forecasts appear in Figures 1 and 2. The forecasts come from Ron Plain, University of Missouri; Lee Shulz, Iowa State University, Jim Robb and the staff of the Livestock Marketing Information Center (LMIC) in Denver and yours truly.

Note that all slaughter figures are for commercial slaughter. Three of the forecasts are quite close for this year but the similarities pretty well end on Jan. 1. Quarterly slaughter forecasts vary by more than 1% for each of the first two quarters and by 1.7% for the third quarter. All analysts expect growth from the second quarter forward.

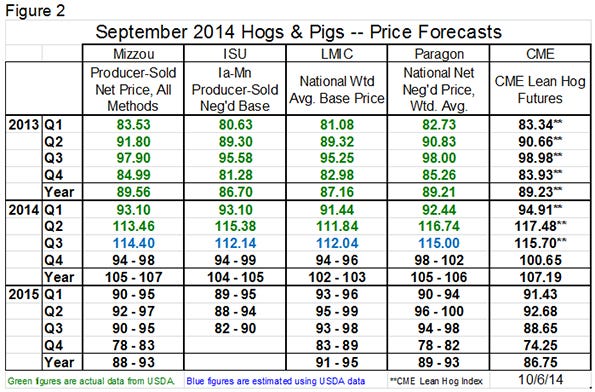

As for prices, the report that almost everyone thought was bearish resulted in only minor changes in analysts’ forecasts. Note that each analyst forecasts a slightly different price so the inherent differences in those prices must be considered when comparing forecasts. That is the primary reason I include last year’s prices in the table since they can be used to get an idea of the differences. The national weighted average base price forecast by LMIC, for instance, was $2 to $2.50/cwt. lower than the series that I and Ron Plain forecast. The Iowa-Minnesota producer-sold negotiated base ran about $0.45/cwt. lower than the national base. Similar difference would be expected this year.

As for prices, the report that almost everyone thought was bearish resulted in only minor changes in analysts’ forecasts. Note that each analyst forecasts a slightly different price so the inherent differences in those prices must be considered when comparing forecasts. That is the primary reason I include last year’s prices in the table since they can be used to get an idea of the differences. The national weighted average base price forecast by LMIC, for instance, was $2 to $2.50/cwt. lower than the series that I and Ron Plain forecast. The Iowa-Minnesota producer-sold negotiated base ran about $0.45/cwt. lower than the national base. Similar difference would be expected this year.

The “bearish” report had little negative impact on Lean Hogs futures as well. After small losses on Sept. 29, the trend has been higher across the board, with strength the greatest for the summer contracts. Those contracts still look underpriced to me as they are currently trading 25-30% lower than the prices we saw last summer. Yes, slaughter will be higher but we don’t expect weights to add much, if any, to that growth and the kind of price declines suggested by futures implies either much larger pork supplies (8-12%) or a significant slacking of demand. The latter is more likely than the former but has, in my opinion, a pretty low probability of actually happening.

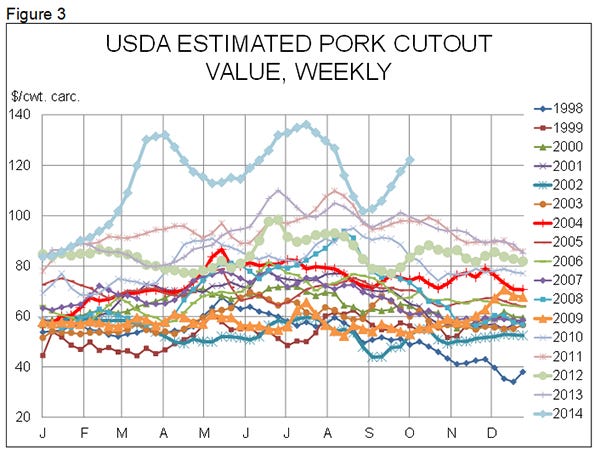

As evidence, consider Figure 3. The chart is clearly very busy but focus first on the remarkable counter-seasonal rally we have seen in the past five weeks. Now search through the tangle of other lines and find another that looks like it. I have bolded four for you to consider: 2002, 2004, 2009 and 2012. In 2002, there was a rally at almost the same time as this year but started that rally at what turned out to be the lowest price of the year in early September. 2004 is noteworthy for the simple lack of any seasonal pattern past the early summer rally of May. It then includes steady to rising prices in the fall months. That year is also noteworthy as the zenith of the Atkins Diet and the positive impact it had on meat demand and prices. 2009 is noteworthy in that prices in December were the highest of the year. Part of that, of course, is due to the normal summer rally being short-circuited by H1N1 influenza concerns. 2012 exhibits much the same price pattern as we have seen in the past five weeks but the fall and rise occurred in mid-August to mid-October.

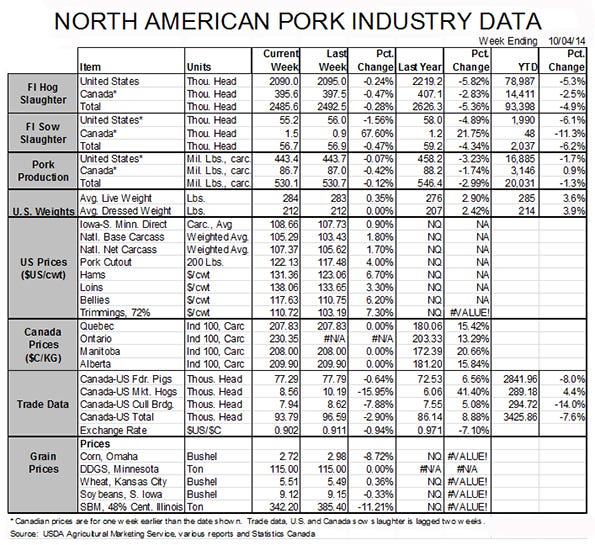

I mention all of these to underscore how unusual this late-summer dip and rally in the cutout value – and hog prices – are in historical terms. The pace of increase did slow slightly last week and I can’t help but believe that it is about to run out of steam. But slaughter dropped back below week-ago levels and fell 5.8% short of year-ago levels last week. The average weight of producer-sold barrows and gilts did gain 0.37 pounds to reach 213.44 pounds carcass weight but that figure is over 3 pounds lower than at the beginning of May. The 0.37-pound increase is paltry compared to a normal seasonal increase. Weights offset only 2.4% of last week’s slaughter increase, leaving pork production down 3.9% year-to-date.

Where to from here? I have to think this counter-seasonal rally is about out of steam. While hog numbers are lower, they will still increase this fall as pigs born in periods of lower porcine epidemic diarrhea virus (PEDV) losses begin to reach market weight. But the rally is great for further-quarter hogs and is, I think, the precursor of more strength next summer. The determining factor of that strength? The answer to everything: PEDV.

You May Also Like

Enter a zip code to see the weather conditions for a different location.