Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

June 24, 2013

We finally have some good news on the hog price front. Last week’s Iowa-Minnesota direct, national base carcass and national net carcass prices all averaged over $100/cwt., carcass, with the net price nearing $103/cwt.

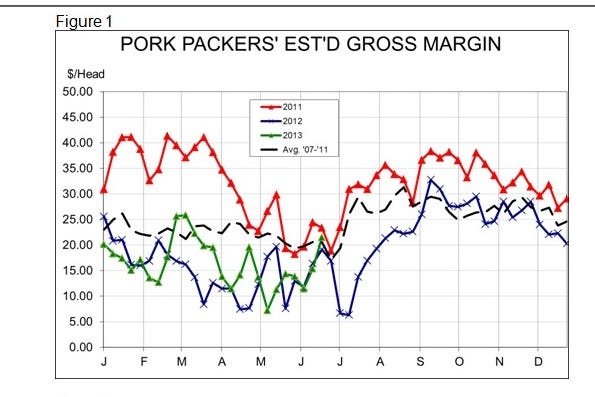

USDA’s estimated cutout value rose over $3 to average $106.79/cwt That improvement takes packers’ “meat margin” back to the positive side of the ledger and, assuming by-product values have remained near the last-reported level of roughly $21/head, puts packer margins back to their 2007-2011 average (Figure 1). That’s very important since packers were not too enthusiastic about slaughtering pigs at gross margins below $15/head. They will be considerably more interested in moving pigs through plants at $20-plus!

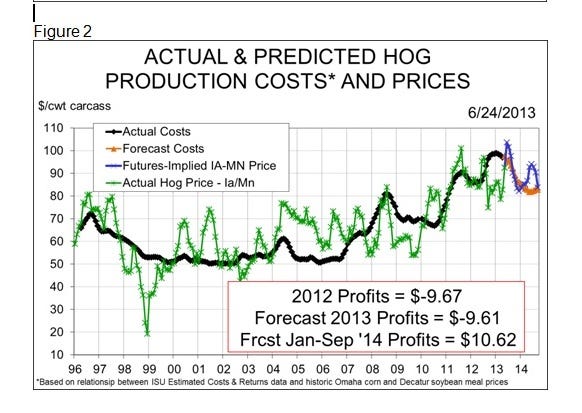

And the margin situation did not just improve for packers. Though some 2 to 2.5 million acres of intended corn acres will not be planted to corn this year, costs continue to slide downward for both the remainder of 2013 and for 2014. My model, based on Iowa State’s Estimated Costs and Returns parameters, now says costs will average $94/cwt., carcass for calendar year 2013 and just under $83/cwt., carcass, for January-September 2014 (Figure 2); 2013 will still be a very negative year with average losses near $10/head, but forecast profits for next year are now above $10/head.

Much of the forward-looking strength for profits is attributable to the sharp rally in live hogs. Cash hogs have risen nearly $10 since mid-May and have carried summer futures up by roughly that amount. But they have also carried December futures up nearly $7/cwt. and June 2014 futures up by nearly $4/cwt.

Like what you’re reading? Subscribe to the National Hog Farmer Weekly Preview newsletter and get the latest news delivered right to your inbox every week!

Combine those market price increases with lower costs and we now see some pretty good opportunities to lock in profits for the coming 12 months. David Ward and Chip Whalen of CIH, LLC in Chicago told those attending the Pork Management Conference last week that the change in lean hog, corn and soybean meal futures has now pushed profit potentials for the next four quarters into roughly the 80th percentile of their historical distribution. That means producers can right now lock in profits that would be as good as or better than the profits in 80% of the commensurate quarters in history. One may not want to hedge them all at that level, but such prospects certainly deserve some consideration, especially given the fact that this year’s crop has not yet been “made.”

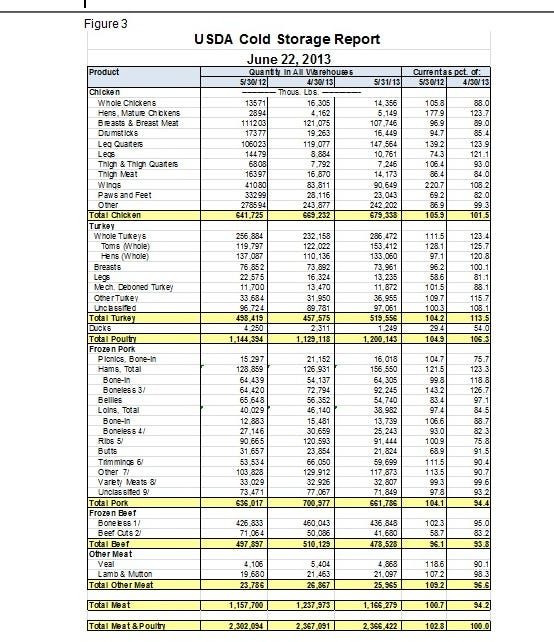

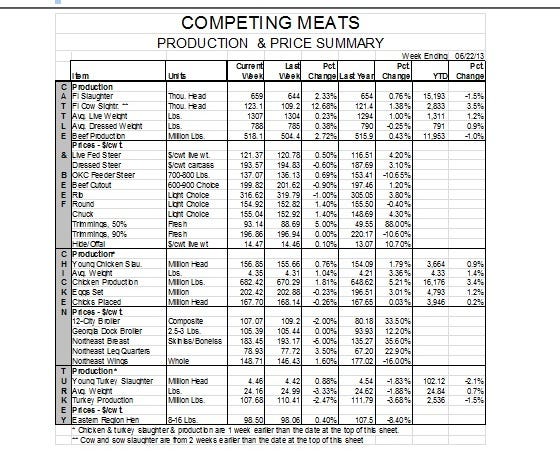

The cash hog rally is even more impressive when one considers that a) exports are still, by all reports, soft and b) frozen imports are large (Figure 3). Friday’s Cold Storage report indicates that May 31 stocks of frozen pork were 4% larger than one year ago. Hams remain as the biggest “problems” (+21% from May 31, 2012 and +23% from one month ago) and “other” pork (+14% from last year). The good news is that inventories declined by 6% during May and that both bellies and loin stocks are lower than last year. In addition, stocks of frozen ribs, which had been burdensome since last summer, are finally being reduced, falling 24% in May to just 1% larger than last year.

Market Drivers

I think the drivers of recent hog prices are two-fold. First, hog supplies have been roughly equal to one year ago and 1-2% lower than I expected based on the March Hogs and Pigs report. My forecasts involved adjustments for last summer’s heat that, as it now appears, may not have been correct. Weights are creeping closer to last year’s heat-induced lower levels and producer-sold barrows and gilts will very likely be heavier this week than they were one year ago. But production is still a bit lower than I had expected at this time.

The second factor, prices of competitor goods, is much larger, in my opinion. Spot prices for boneless/skinless chicken have been near $2/lb. The choice-grade beef cutout moved barely below $200/cwt. last week after spending the past six weeks above that level. Wholesale prices of “middle meats,” such as loins and ribs, led the increase in the cutout value. Higher priced loins and ribs mean pricey T-bones, porterhouses, strips and ribeyes. It appears that the National Pork Board’s efforts to rename pork cuts after their beef corollaries could not have come at a better time.

You might also like:

NPPC Comments on Failed Farm Bill

Farm Bill’s Demise Highlights Divide between Urban, Rural America

You May Also Like

Enter a zip code to see the weather conditions for a different location.