Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

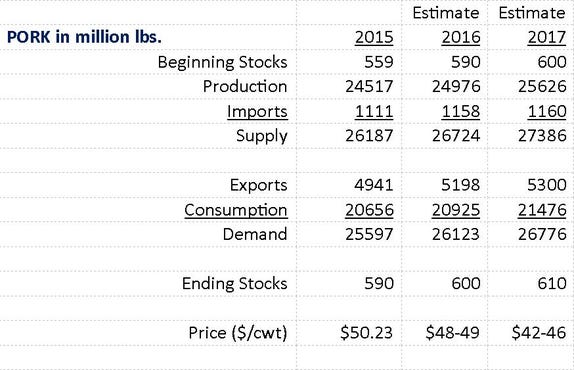

USDA quietly lowers the average price for 2017 by roughly $10 per pig compared to this year.

June 13, 2016

I love the World Pork Expo. We look forward to it every year. This year’s turnout was fantastic and the lack of rain submerging electrical cords along tent row was an added bonus. Some takeaways from questions posed to us over the past week:

What accounts for the 100% jump in the price of oil? The impact of macro-economic issues (an inflection point may have been the Chinese currency devaluation in August of 2015) have impacts on our markets that can befuddle fundamental traders. Money flow into the commodity space has totaled $55 billion in the last four months. Of that, our ag sector has been the recipient of $8 billion in new activity. This helps explain the 100% jump ($25 to $50/barrel) in the price of oil and how beans have managed to rally $2/bu. with minimal fundamental influence. Do not cast this aside, it will continue to play a role. When Janet Yellen is on TV, pay attention.

Where are producers finding significant opportunity? The world is still interested in United States agriculture. Mergers and acquisitions on a macro-level have seen significant growth as exemplified by recent activity such as DuPont/Dow, Monsanto/Bayer and Syngenta/China. There are opportunities in the smaller scale, too. Our global analyst continues to note the common themes and stories of increased interest in US ag operations by foreign entities. The common story does not focus on owning bean ground in central Iowa; rather it features controlling an integrated process that can deliver protein to the buyer. Smithfield was purchased a few years ago by a Chinese entity. This same spirit (the acquisition of vertically integrated systems) is alive and well for foreign investors. Individual producers do not have to reinvent the wheel here— being a cog in a larger system may be enough to reap the rewards. Pension funds are still interested in farm ground, others want the protein machine. This opens producers up to a completely different field of opportunities.

Where can producers make themselves attractive to packers? The sentiment of vertical integration is not confined to foreign acquisitions. Transparency—The “Need to Know”—motivates the packing industry as they sort dance partners for the future. This week, more than one packer indicated that a producer with his own mill is a benefit. The ability to track and trace – whether for an ABF program or other requirement – has shifted from producer affidavits to feed verification. Producers can leverage a huge opportunity here, in my opinion. Several World Pork Expo exhibitors showcased software and hardware to meet this demand. This one seems “realizable” to me; we have the technology to meet the requirement.

To expand or not to expand? Our Field of Dreams mentality of “if-you-build-it-they-will-come” is alive and well in the pork industry. The addition of the new plants is generating an irresistible euphoria, triggering partnerships among cash affluent pork producers, and low-interest lenders at a time when alternate returns for money in your pocket is roughly zero. This is our time to expand and improve. We have money flowing into the sector, a building influx of new sow farms and multiplication, and refurbishment of old buildings. Bona fide stories of 30+ PSY continue to ramp up amortization schedule, and the promise of further productivity gains keeps the dream alive.

Let’s take a step back and analyze this scenario outside the bloat of a couple of days of all-you-can-eat ribs, sausage and pulled pork.

The short story

USDA lowers the average pork price by $10/pig from 2016 to 2017

Discrepancy of $25/pig between CME values vs. USDA predictions

Report was friendly beans, neutral corn, disaster for wheat

Hard to break markets until July/August timeframe

Watch for potential deliveries against July board by commercials

Producers should plan on another 30-60 days of market volatility

The long version: We had a USDA report out this past Friday that was mainly focused on the grain sector. What may have been overlooked in the wake of the grain activity was the quiet way the USDA pushed out a new price estimate for pork for calendar year 2017, lowering the average price by roughly $10/pig compared to this year. Production was raised (remember, we have a Hogs and Pigs report out on the 24th of this month. Hint.) which largely fell on the shoulders of the domestic consumer for disappearance. Remember, demand is disappearance at a price. Encouraging the U.S. consumer to eat more will have to require an incentive, the USDA says that will come in the form of lower prices.

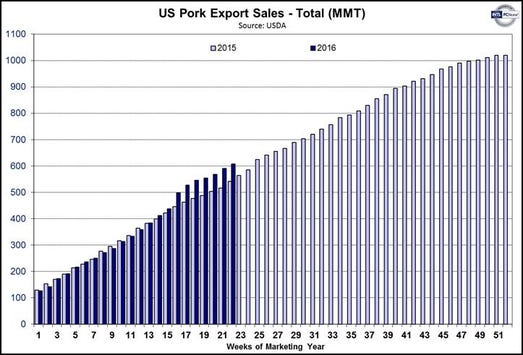

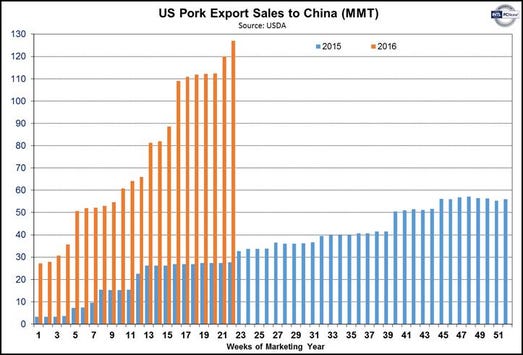

Remember, this price is in live terms so you have to convert to carcass for comparison to the CME. As of Friday’s close, the 2017 string on the board averaged roughly $71.50 for the year. Converting the USDA data to carcass yields an average estimate of just shy of $59. Hmmm. This is a discrepancy of about $25/pig between what you can hedge on the CME versus where your government is predicting prices. I am not saying one is “right” and the other is “wrong”, it just seems to me that this is a huge difference in perception with the advantage available to the pork producer to hedge the spread. Put another way, it would really stink if this were the other way around and the USDA was predicting higher prices than the market was allowing and you wanted to execute on the USDA values – there would be no vehicle to do so. The key variable in the data is likely our favorite five-letter word – China. The futures market is a buzz with the prospects of the presence of China while the USDA regression is likely slower to incorporate the potential shift. I have attached a couple of charts referencing the export pace of pork to the world and China, you can visually witness the reason for the hyperventilation. Exports to the world are pretty mundane, China is a rousing success.

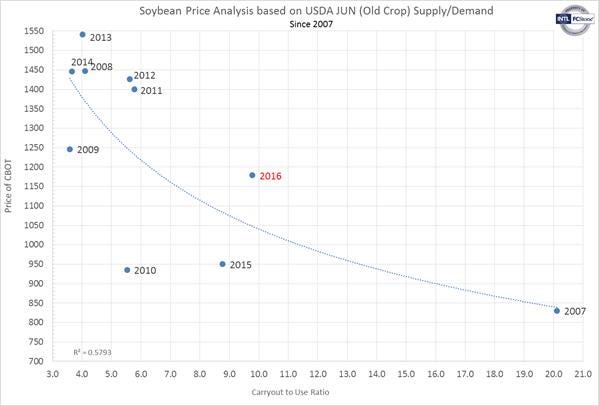

My take home from the Friday grain report: we substantiated the balance tables the trade had been anticipating. From the outside looking in, it would appear to be a bullish report on beans, neutral to bullish for corn, and an unmitigated disaster for wheat prices. In my opinion, it is neutral for corn, tenuous for soy, an unmitigated disaster for wheat. We will likely not talk much about the report from here forward, focus will be on the weather. As I write this, there is a system moving through Iowa just south of Interstate 80 that was NOT on the maps yesterday. A moody, energy-filled atmosphere can kick off a storm at any point.

This has always been a new crop story. We just posted a 260 carryout in beans next year with March 31st acres and trend yield. What is it with 85 million planted and a 48 yield (+200 million from 260) or 85 million acres and a 45 yield (-25 million from 260). So for now we have a 235 to a 460 carryout range. While it may be too soon to get a good reading on July/August US weather, there are some weather guys who are suggesting a less-than-expected problem across the US this summer as what needs to be setting up in the models is not happening. This would suggest the heat and dryness across the US during the critical pollination and flowering time frame may not as dire as thought from 30-60 days ago. This does not mean we are out of the woods, quite the opposite. With the increase in demand for US old crop due to South American production problems, the cushion of “OK or not OK” for US new crop yields have shrunk dramatically. So while we may be trying to moderate US summer weather, even a small problem can become an issue.

I believe it will be hard to break this market until we get into the July/August timeframe. The June 30 stocks and acres report could be the first real jab if the above-mentioned acres are realized for beans. In addition, I have been harping to whoever will listen about the potential for deliveries against the July board by commercials that have had their head handed to them by the funds. They have a shot at redemption, I suspect they will take it. Fund longs will not be a ready to bail until they get a significant signal to leave the position, especially if the Fed does not hike and we see a drop in the US dollar. My Right Wing Buddy in Chicago believes that, at some point, the European Central Bank and Bank of Japan step in to weaken their currency. Bottom Line: we should see escalated market volatility over the next 30-60 days, lets get ourselves positioned accordingly.

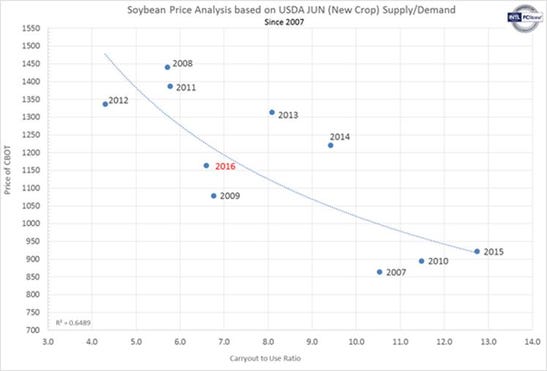

These two charts may indicate that old crop soybeans are over-valued and new crop under-valued, strictly looking this history alone. May need more premium in new crop.

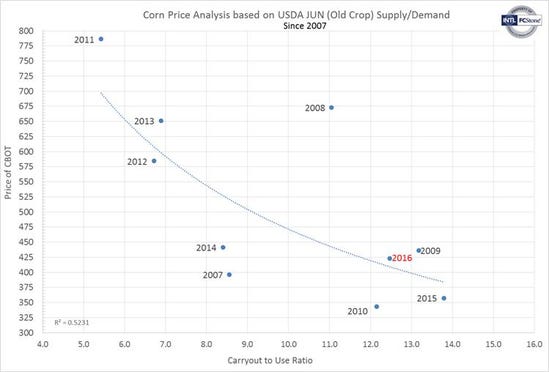

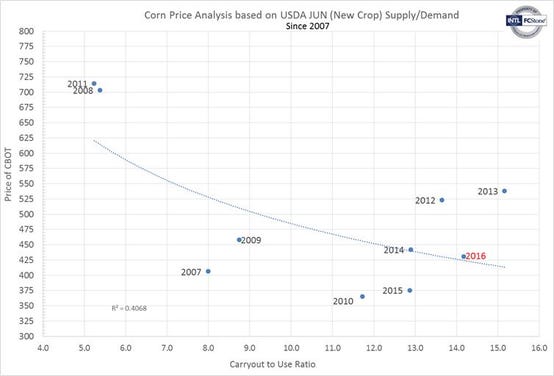

Corn looks relatively fairly valued based on the historical data and where the market ended Friday.

Comments in this article are market commentary and are not to be construed as market advice. Trading is risky and not suitable for all individuals.

You May Also Like

Enter a zip code to see the weather conditions for a different location.