Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

Should hog prices be higher? Probably; competition drives hog prices and profits create competition. There’s a reason four packing plants are in some stage of construction and a fifth is in the works.

August 1, 2016

It’s always nice to get something right, but this is one time when I wish I had been wrong. I’ve been warning for some time that I could not, based on the supply data, get cash hogs anywhere near what was, to me, the inflated level of CME Lean Hogs futures.

The futures market has solved the difference by coming back to — and in some cases beyond — the levels that I was forecasting. And last week was a tough week for pork markets as the complex continues to adjust to the reality of big hog numbers. Our colleague Dennis Smith laid out last week a number of factors that could drive a late-summer hog rally — and he is right that those things could push prices higher. The question is whether enough of them will happen to thwart the negative factors that have developed recently.

One thing is for sure: Any cash hog rally from $83 will not reach any lofty heights since the launch will commence at a point that once was in the basement. Let’s review what has happened.

Be more like Doug This was a man of true character; a gentle person whose kindness overshadowed even his own considerable intellect. My pastor started a funeral sermon for one of the revered statesmen of our church a few years ago with “Lord, let me be more like Bruce.” And Bruce Kiehl was such a person that everyone in attendance echoed that prayer. In the wake of Doug’s death, many of us will — as we should! — pray “Lord, let me be more like Doug.” Such is indeed a noble calling. This was a good, good man. My thoughts and prayers are with Doug’s family and long list of friends who feel just like I do today. — SRM |

The big drivers of the $6.36 per hundredweight drop in the average weekly cutout value were bellies and hams whose primal cutout values dropped by 14.7% and 13% in just one week. Those are big declines for products that represent 40% of the pork carcass. The belly decline resulted from the liquidation of large (but not huge) freezer inventories that began in June. With more hogs and more bellies on the way and Labor Day within sight, it was time to move those inventories. But just how much impact will these product price declines have on hogs?

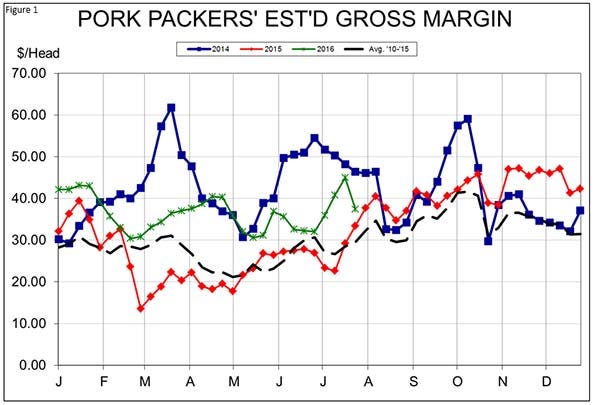

Various direct hog prices declined by 3 to 5% last week even as the cutout fell by 7.1%. The shock absorber in this case was, of course, packer margins (see Figure 1). There appears to be plenty of room to absorb some shocks here. Our computations of gross packer margins indicate that they have exceeded year-ago levels in every week so far in 2016. And they were not that bad in 2015 except for March and April when the West Coast port backlog was being rectified. Note as always that these are gross margins calculations (meat value + byproduct value - hog cost) and that packers must pay all non-hog costs before arriving at a “bottom line” net profit figure. But how much have those other costs changed over the past year or two years, especially with the decline in energy values?

We doubt that the change has been much and a steady recovery in byproduct values is contributing to a very healthy situation for packer gross margins. The Livestock Marketing Information Center’s weekly estimate of byproduct or drop values has grown from just $13.04 per head back in January to over $21 per head since late-June. That is a far cry from the $29.56 fetched for byproducts the week of July 26, 2014, but it is a substantial improvement at a time when the spread between hog and cutout values is still very wide.

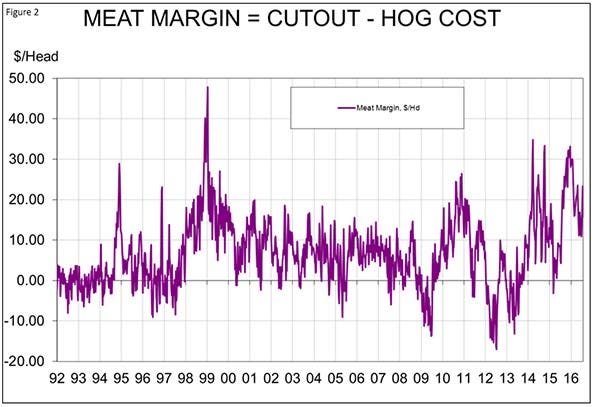

The cutout-to-hog spread or what I call the meat margin has had a remarkable run the past three years, reaching $30 per head on several occasions. The last time that happened was in 1998. Porcine epidemic diarrhea virus-related supply concerns were the spark for this growth in meat margins which have remained strong except for that first quarter of 2015 and the aforementioned dock work problems. These historically large spreads were due, in part, to those lagging byproduct values so I expect them to decline as more of the packers’ margins needs are met by organ meats, head products and various other “everything but the squeal” items.

So should hog prices be higher? Probably. But competition drives hog prices and profits create competition. There’s a reason four packing plants are in some stage of construction and a fifth is in the works. Gross margins average $17.38 per head from 1992 through 2009, a period that included the banner years of 1994 and 1998. But gross margins averaged $29.75 per head from 2010 through 2015 and have averaged $36.01 so far in 2016. More shackle spaces will almost certainly squeeze those margins to the benefit of both producers and consumers beginning in late-2017, but large hog supplies this fall will likely leave packers in the driver’s seat.

You May Also Like

Enter a zip code to see the weather conditions for a different location.