Subscribe to Our Newsletters

National Hog Farmer is the source for hog production, management and market news

March 14, 2016

The demand news for January was a mixed bag.

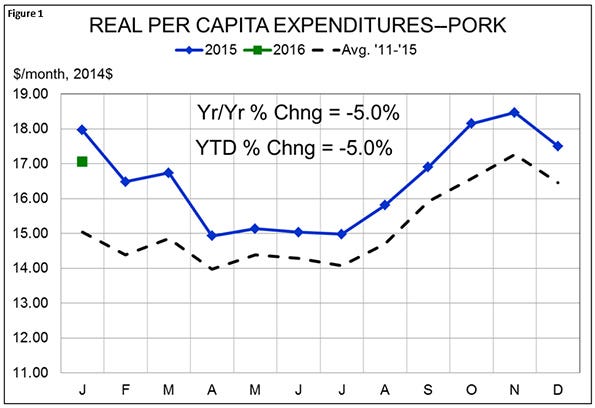

Real per capita expenditures for pork, the metric I use to represent the state of consumer-level pork demand, was down 5% from one year ago but still 13.5% larger than the 2011-15 average for January (see Figure 1). The first number is not good news while the last number keeps this year’s figure of $15.04 per person in some historical perspective. Further, we also know that RPCE figures for January through March 2015 were likely artificially high due to the West Coast port slowdown that forced product on to the U.S. market. That drove up per capita consumption, but likely did not impact retail prices since retailers knew that the wholesale price decline caused by the exports difficulties would be temporary. They held the line on retail prices and the combination of those strong prices and higher per capita consumption pushed the 2015 first quarter figures higher than they otherwise would have been. I won’t be surprised if February and March RPCE figures for this year are lower than last year as well.

That drove up per capita consumption, but likely did not impact retail prices since retailers knew that the wholesale price decline caused by the exports difficulties would be temporary. They held the line on retail prices and the combination of those strong prices and higher per capita consumption pushed the 2015 first quarter figures higher than they otherwise would have been. I won’t be surprised if February and March RPCE figures for this year are lower than last year as well.

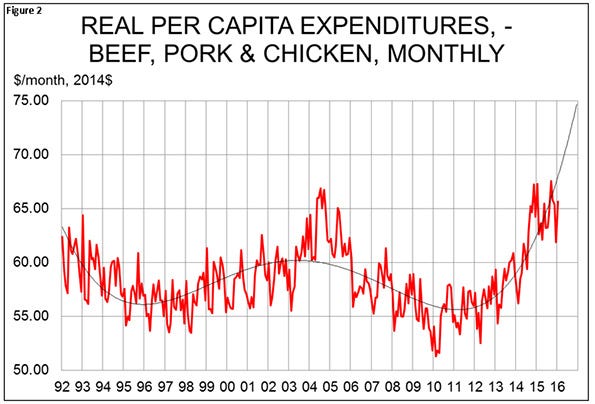

When we focus on that longer historical perspective, I think the meat demand world is still quite good. January’s RPCE for beef, pork and chicken (recall that I do not include turkey due to USDA providing only a whole-bird retail price) was 2.5% lower than one year ago — again, not a good number. But consider the long-term trend shown in Figure 2. The December and January observations are indeed below the polynomial trend line computed for this chart by Excel. But note that, except for the remarkable totals of 2014, the trend line would be somewhat flatter and these last two months would have been only slightly below it — if they were below it at all.

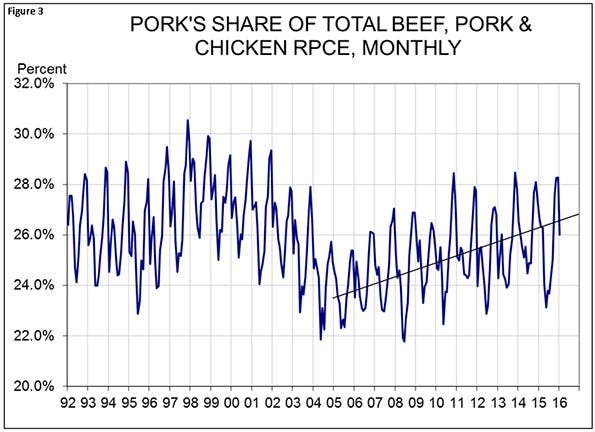

Finally, pork has been more than merely “along for the ride” as meat and poultry demand has grown in recent years. Figure 3 shows that pork’s share of three-species RPCE has grown steadily over the past 10 years. While there is significant seasonal variation, the uptrend is clear. Increasing pork’s share of total RPCE is an important facet of the National Pork Board’s five-year strategic plan and it recognizes that, while being along for the ride is good, being in the driver’s seat is better. So what is the prognosis for pork demand? I remain in the camp that this growth trend will likely slow, but that pork demand has made some gains that it will not relinquish in the absence of some severe product quality or wholesomeness scare. Consumer preferences have shifted back toward meat in spite of what many thought were almost damning animal welfare issues that, at least to us, seemed to dominate the news. While pork producers and activists get excited about such issues and occurrences, it appears from these data that the vast majority of consumers either does not know about them or does not care. The positives of dietary protein and lessened concerns about fat and cholesterol have also played a role in this demand resurgence.

So what is the prognosis for pork demand? I remain in the camp that this growth trend will likely slow, but that pork demand has made some gains that it will not relinquish in the absence of some severe product quality or wholesomeness scare. Consumer preferences have shifted back toward meat in spite of what many thought were almost damning animal welfare issues that, at least to us, seemed to dominate the news. While pork producers and activists get excited about such issues and occurrences, it appears from these data that the vast majority of consumers either does not know about them or does not care. The positives of dietary protein and lessened concerns about fat and cholesterol have also played a role in this demand resurgence.

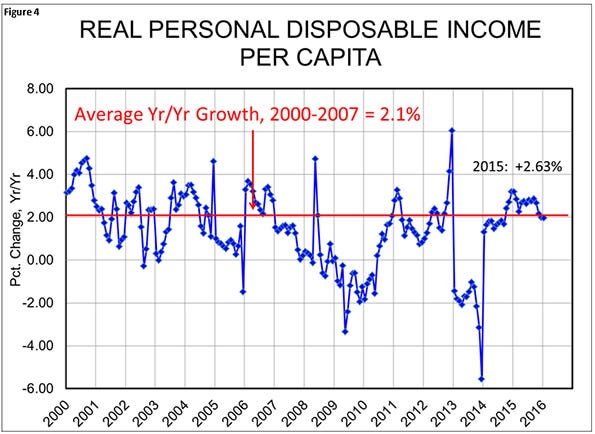

So has the economy. It is no accident that RPCE has been growing steadily since 2010 when the economy finally bottomed out from the financial crisis of 2008-09. From consumers’ perspectives, even the turnaround did little for buying power through 2013. Real personal disposable income per capita (see Figure 4) showed some signs of life in 2014 and then had its best year since 2006 last year, with the average year-on-year increase hitting 2.6%. January’s 1.98% is a bit of a concern, but this measure which represents the amount of money per person that is left after all taxes are paid has improved sharply. The longer that it stays in the 2% year-on-year growth range, the more comfortable consumers will be that the income gains will last and thus support more spending.

There is an even longer-impact issue here; every business wants to walk a tightrope between providing their customer the best value possible and extracting the most value possible from that customer when selling them a product. If you have a great product, you want to capture value and, in truth, the customer will only pay you as much value as you deliver — and ask for. That last point is important in the wake of record retail meat and poultry prices. Consumers never revealed that they would be willing to pay an average price of more than $6 per pound for beef and $4 per pound for pork. A major reason is that neither the beef industry nor the pork industry had ever asked them to do it! We have now and they have now.

The question now is “How do we create enough value in the eye of the consumer that they will pay these newly discovered prices again and regularly?” They did it the first time because supplies were tightened. But now that they will, and we know that they will, pay that much, what must be done to make those now-familiar prices “reasonable” to them every day? It’s not enough to just ask, we must also deliver. I know it’s a challenge but I believe it is one that is well worth it!

You May Also Like

Enter a zip code to see the weather conditions for a different location.